Buying property with savings is more common than many people think. If you have enough money set aside, you may be wondering whether you can buy a house with cash, whether UK sellers will accept it, and whether the process is as simple as handing over money and getting the keys. The short answer is yes, you can buy a house with cash in the UK, but it does not mean bringing a suitcase full of banknotes to the estate agent.

In property terms, buying with cash usually means you are paying for the home without a mortgage. The money still needs to go through the proper legal and banking steps. That means proof of funds, solicitor checks, anti-money laundering checks, and secure transfer of money through the right channels.

Many buyers like the idea of avoiding mortgage stress, monthly repayments, and long approval delays. Others want to move quickly, bid more strongly, or invest in property without borrowing. This is why cash purchases remain popular with first-time buyers who have saved well, downsizers, investors, and overseas buyers.

What Does “Buying a House with Cash” Mean in the UK?

When people talk about a cash buyer UK property deal, they usually mean someone who can pay the full price without a mortgage. In simple terms, the buyer already has the money available and does not need to borrow from a lender.

That does not always mean physical cash. In almost every case, the money comes from a bank account, savings, an inheritance, investments, or another legal source. The solicitor then handles the money safely during the purchase.

A cash buyer may be:

- Someone is using personal savings

- An investor buying property outright

- A person using inheritance money

- A homeowner selling one property and buying another without borrowing

- An overseas buyer transferring funds into the UK

Who Qualifies as a Cash Buyer?

A cash buyer is anyone who can complete the purchase without a mortgage. Sellers and agents often prefer cash buyers because they are usually faster and less likely to face finance delays.

This can include:

- UK residents with strong savings

- Buy-to-let investors

- Retirees using pension or sale proceeds

- Inheritance recipients

- Overseas buyers who transfer funds legally

Can You Use Physical Cash to Buy Property?

In practice, no, not in the normal sense. UK property purchases are not done by handing over bags of notes. Large cash payments pose serious money laundering concerns, so banks and solicitors will usually not accept them.

The money must be traceable. That means it should move through the banking system with a clear paper trail. This helps prove that the funds are legal and reduces the risk of fraud.

Can You Legally Buy a House with Cash in the UK?

Yes, it is completely legal to buy a house with cash in the UK. In fact, it happens every day. The key point is that the money must be genuine, traceable, and properly checked.

The legal process is guided by solicitors, estate agents, and financial regulations. These rules are in place to stop fraud, tax evasion, and money laundering.

Why Solicitors Ask for Proof of Funds

Your solicitor will usually ask for proof of funds and UK property checks before moving forward. This is normal.

They may ask for:

- Recent bank statements

- Savings records

- Investment account statements

- Inheritance documents

- Proof of a property sale

- Gift letters, if money came from the family

This is not meant to be awkward. It is simply part of the UK conveyancing process.

Anti-Money Laundering Checks Explained

AML stands for anti-money laundering. These checks help confirm that the funds used for the purchase are from a legal source.

Solicitors and estate agents must look out for suspicious activity. If something does not add up, they may ask more questions or report it. This protects everyone involved in the deal.

These checks can include:

- Confirming your identity

- Reviewing your source of funds

- Checking the path money has taken

- Reporting suspicious transactions if needed

Can Overseas Buyers Purchase with Cash?

Yes, overseas buyers can buy UK property with cash too. However, they may face extra checks and extra paperwork.

If you are buying from abroad, expect:

- Currency transfer checks

- Identity verification

- Proof of income or savings source

- Possible tax and legal questions depending on your situation

The process is legal, but it must be carefully managed.

Advantages of Buying a House with Cash in the UK

Many people prefer cash purchases because they can make the whole process smoother and less stressful. In the UK property market, a cash buyer often stands out.

Faster Property Transactions

One of the biggest benefits is speed. Without a mortgage, you do not need to wait for lender approval, valuation checks, or mortgage paperwork.

This can make the purchase quicker because:

- There is no mortgage application

- Fewer parties are involved

- Conveyancing can move faster

- Sellers often feel more confident

If you want to move quickly, this is a major advantage.

Stronger Negotiating Power

Cash buyers often have more bargaining power. Sellers may accept a slightly lower offer if they know the sale is more likely to complete.

Why? Because a cash offer often feels safer. There is less risk of the deal falling apart due to financing issues.

This can help you:

- Negotiate a better price

- Compete more strongly in a hot market

- Appeal to sellers who need certainty

No Mortgage Interest Payments

When you buy without borrowing, you avoid mortgage interest. That can save a lot of money over time.

You also avoid:

- Monthly mortgage repayments

- Lender fees

- Mortgage arrangement charges

- Some ongoing borrowing costs

For buyers who want lower monthly expenses, this is a big plus.

Lower Risk of Property Chain Collapse

A property chain occurs when several people are buying and selling homes simultaneously. If one deal fails, the whole chain can break.

Cash buyers reduce this risk because they do not have to wait for mortgage approval. Sellers like that. It gives them more confidence that the sale will be completed.

Potential Auction Opportunities

Cash buyers often do well at property auctions. Auction sales move quickly, and buyers usually need funds ready quickly.

If you have cash available, you may be able to:

- Bid with confidence

- Complete faster

- Buy properties below market value

- Act on renovation opportunities

Disadvantages and Risks of Buying with Cash

Even though cash buying has many benefits, it is not perfect. You should think carefully before tying up a large amount of money in one property.

Reduced Liquidity

When you put most of your money into a house, that money becomes harder to access.

This can be a problem if you need:

- Emergency funds

- Money for business

- Help with family costs

- Flexibility for future investments

A home is valuable, but it is not easy to turn into cash quickly.

Lack of Mortgage Protection

Mortgage lenders often insist on checks, valuations, and surveys. Cash buyers sometimes skip these steps because they feel the deal is simpler.

That can be risky. Without proper inspections, you might miss hidden problems such as:

- Damp

- Structural damage

- Roofing issues

- Drainage problems

Fraud and Scam Risks

Cash buyers can sometimes attract fraudsters because the money is ready and available.

Watch out for:

- Fake sellers

- Property identity fraud

- Unregulated legal help

- Pressure to transfer money too quickly

Using a regulated solicitor is essential.

Opportunity Cost

Money spent on a house cannot be used elsewhere. That is called opportunity cost.

For example, you might have earned more by:

- Investing in another property

- Putting the money into savings

- Using a business investment

- Keeping funds available for inflation or future opportunities

A house can be a strong asset, but it is still worth comparing your options.

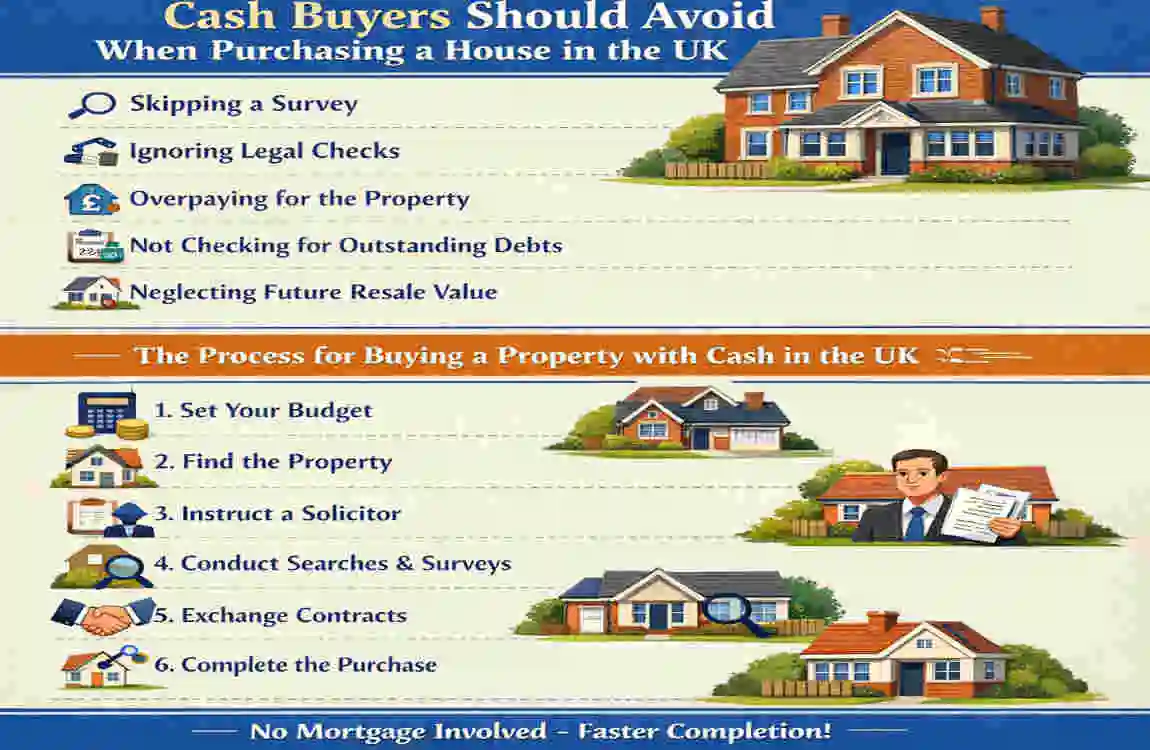

Step-by-Step Process of Buying a House with Cash in the UK

If you are serious about buying a UK property in cash, it helps to understand the full process before you start.

- Set your budget

- Gather proof of funds

- Find the right property

- Hire a conveyancing solicitor

- Make an offer

- Arrange searches and surveys

- Exchange contracts

- Complete the purchase

Determine Your Budget

Start with the full cost, not just the purchase price. You need to include legal fees, stamp duty, survey costs, and any repairs.

Gather Proof of Funds

Prepare bank statements, savings evidence, inheritance records, or investment documents. This will help your solicitor move faster.

Find a Property

You can search through estate agents, property portals, or auctions. Think about location, condition, and long-term value.

Hire a Conveyancing Solicitor

A solicitor handles the legal side of the sale. They verify ownership, review contracts, and ensure the title is transferred properly.

Choose someone who is regulated and experienced in buying property in the UK without mortgage rules.

Make an Offer

Your offer should be realistic. If you are a cash buyer, make that clear. Sellers often value speed and certainty.

Property Searches and Surveys

Even with cash, do not skip checks.

These may include:

- Local authority searches

- Environmental searches

- Structural surveys

- Title checks

Exchange Contracts

At this stage, the deal becomes legally binding. A deposit is usually paid, and both parties commit to completing the project.

Completion Day

On completion day, the money is transferred, the seller receives the funds, and you get the keys. The property is then registered in your name.

How Long Does a Cash House Purchase Take in the UK?

A cash purchase is usually faster than a mortgage purchase. In many cases, it can take 2 to 8 weeks, depending on the property and legal work involved.

A mortgage purchase often takes 2 to 4 months or more.

What Affects the Timeline?

The speed depends on:

- How quickly can proof of funds be provided

- Whether searches are needed

- How busy the solicitor is

- Whether there is a property chain

- Whether legal issues appear during checks

A cash deal can still be delayed if the paperwork is incomplete, so speed is not automatic.

Costs Involved When Buying a House with Cash

Even without a mortgage, buying a home is not free. There are still several costs to plan for.

Cost Type: What It Covers: Typical Note

Stamp Duty Land Tax: Tax on property purchases, depending on price and buyer status.

Solicitor Fees , Legal work, and conveyancing vary by firm

Property Survey Checks the condition of the home , from basic to detailed reports

Land Registry Fees: Registers you as the owner. Usually modest

Currency Exchange Costs for overseas buyers depend on exchange rates

Stamp Duty Land Tax (SDLT)

Stamp duty may still apply even if you pay with cash. The amount depends on the property price, whether it is your main home, and whether you already own other property.

Solicitor and Conveyancing Fees

You still need legal help. Fees vary, but it is worth paying for proper service rather than risking mistakes.

Property Surveys

A survey helps you understand the condition of the home. A cheap survey may be enough for a newer property, but older homes may need a more detailed inspection.

Land Registry Fees

Once the purchase is complete, the property must be officially registered in your name.

Currency Exchange Costs for Foreign Buyers

If you are bringing money into the UK from another country, exchange rate changes and transfer fees can affect your final cost.

Is Buying a House with Cash Better Than Getting a Mortgage?

The answer depends on your goals. There is no single right choice for everyone.

Cash Purchase Mortgage Purchase

Faster process , Longer approval process

No interest , Monthly repayments

Stronger negotiation , lower upfront cash needed

Simpler deal structure keeps more savings available

When Buying with Cash Makes Sense

Cash often makes sense for:

- Investors

- Retirees

- Downsizers

- Buyers who want speed

- Buyers who want to avoid debt

When a Mortgage May Be Better

A mortgage may be better if you want to:

- Keep your savings liquid

- Spread the cost over time

- Build credit history

- Use money for other investments

For many buyers, the choice depends on cash flow and long-term plans.

Can You Buy Property at Auction with Cash in the UK?

Yes, and auction luxury houses often prefer cash buyers. That is because auction sales move fast and need quick completion.

If you buy at auction, you usually need to be ready to move quickly. This makes cash especially useful.

Auction Deposit Requirements

You may need to pay a deposit straight away, often on the day of the auction. You also need to complete within the required timeframe, which is often short.

Due Diligence Before Bidding

Never bid without checking:

- The legal pack

- Property condition

- Special auction terms

- Estimated repair costs

Auction properties can be good deals, but they can also hide expensive problems.

Common Mistakes Cash Buyers Should Avoid

Cash buyers sometimes think they can skip the usual checks. That can be a costly mistake.

Skipping Surveys

A house may look fine at first glance, but hidden damage can be expensive. Always inspect before buying.

Ignoring Hidden Costs

Do not focus only on the asking price. Think about tax, repairs, legal fees, and moving costs.

Failing AML Checks

If you cannot clearly show the source of the money, the deal may be delayed or blocked.

Rushing Into Property Auctions

A quick sale can be tempting, but speed should never replace careful research.

Not Using a Solicitor

Trying to handle everything yourself is risky. A solicitor protects you and keeps the purchase legal.

FAQs About Buying a House with Cash in the UK

Can you buy a house with physical cash in the UK?

Not in the normal way. UK property purchases are usually made by bank transfer, not in cash.

Do cash buyers pay stamp duty?

Yes, usually they do. Stamp duty depends on the property and the buyer’s circumstances, not on whether you use cash or a mortgage.

Is buying with cash faster?

Usually, yes. There is no mortgage approval stage, so that the process can move more quickly.

Can foreigners buy UK property with cash?

Yes, foreign buyers can purchase property in the UK with cash, but they may face extra checks and paperwork.

Do I still need a solicitor if I pay cash?

Yes. A solicitor is still needed to handle the legal transfer and protect your interests.

How do solicitors verify cash funds?

They may ask for bank statements, investment records, proof of inheritance, or other documents showing the source of the money.

Are cash buyers more attractive to sellers?

Usually, yes. Sellers often prefer cash buyers because they reduce the risk of delays or financing failures.

Can you negotiate property prices better with cash?

Often, yes. A cash offer can give you more leverage, especially if the seller wants a quick and certain sale.

Yes — you can buy a house with cash in the UK. Below is a short SEO-friendly informational table summarising what cash buying means, benefits, drawbacks, proof needed, and the typical process