If you’re asking how much you need to earn to buy a 500k house in the UK, this guide breaks down everything you need to know in simple terms. A £500k property is no longer unusual in many parts of the UK, especially in London, the South East, and other high-demand areas. But the real question is not just whether you can buy it — it is whether you can comfortably afford it?

That depends on more than your salary. Lenders look at your deposit, credit history, debts, monthly spending, job type, and interest rates. On top of that, buying a home comes with additional costs such as stamp duty, legal fees, surveys, and moving expenses. Many buyers focus only on the mortgage and forget the rest.

How Mortgage Affordability Works in the UK

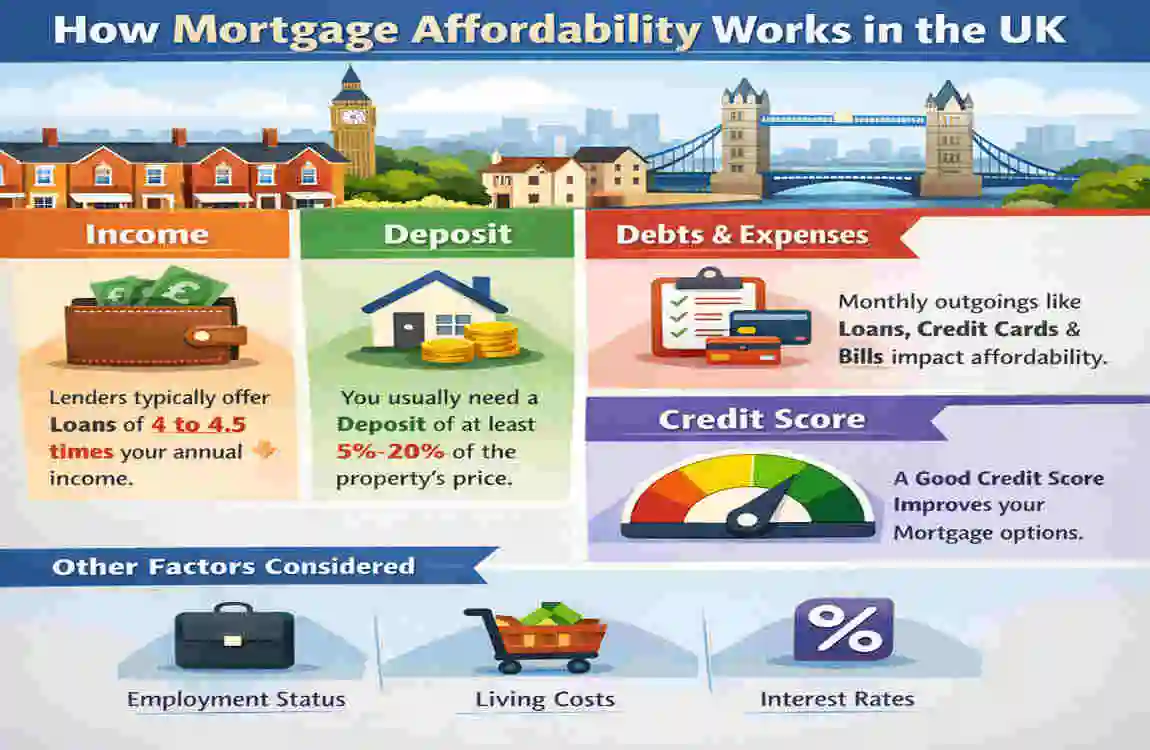

Buying a home in the UK starts with mortgage affordability. This is the lender’s way of checking whether you can handle the loan now and in the future.

The Mortgage Income Multiplier Explained

Most lenders use an income multiple to estimate how much you can borrow. In simple terms, they may offer around:

- 4 times your salary

- 4.5 times your salary

- Up to 5.5 times salary for some high earners or certain professions

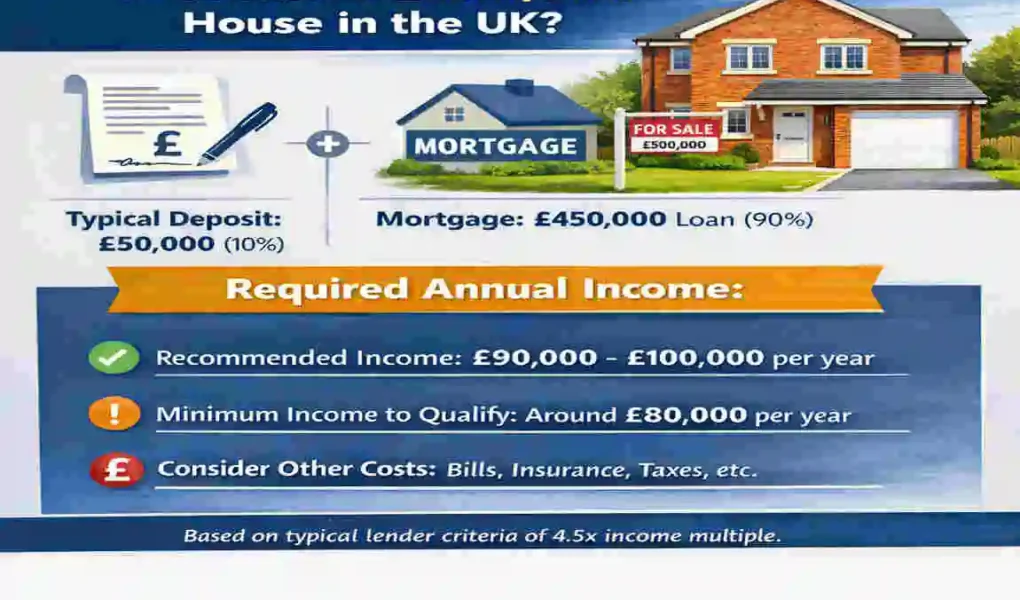

So if you earn £100,000, a lender might offer a mortgage of around £400,000 to £450,000, depending on your financial profile.

That means the deposit becomes very important. If the luxury house costs £500,000 and you can borrow £400,000, you would need a £100,000 deposit.

Why Lenders Don’t Just Look at Salary

Your income matters, but lenders also want to know how safe you are as a borrower. They will check:

- Credit score

- Existing debt

- Monthly outgoings

- Number of dependents

- Employment type

- Bonus or commission income

This is why two people on the same salary may get very different borrowing offers. One person may have car finance, credit card debt, and a large monthly spend, while the other may have very few commitments.

Mortgage Stress Testing

Lenders also run a stress test. This means they check whether you could still afford repayments if interest rates rise. So even if your salary looks strong, your borrowing may be lower if the lender thinks your budget is too tight.

This is one reason buyers are sometimes surprised. You may think you can borrow enough, but the lender may decide otherwise based on your full financial picture.

How Much Salary Do You Need for a £500k House?

This is the section most buyers want to know. The answer depends on the size of your deposit and the mortgage lender’s rules.

Typical Deposit Requirements

A bigger deposit means you need to borrow less, which improves your chances of approval.

Deposit %Deposit Amount Mortgage Needed

5% £25,000 £475,000

10% £50,000 £450,000

15% £75,000 £425,000

20% £100,000 £400,000

A 20% deposit is usually much better for affordability, as it reduces the loan amount and often gives you access to better rates.

Salary Needed Based on Mortgage Multiples

Here is a simple breakdown of the income needed based on common lending multiples.

Mortgage Amount4x Income4.5x Income5x Income

£475,000 £118,750 £105,555 £95,000

£450,000 £112,500 £100,000 £90,000

£400,000 £100,000 £88,888 £80,000

Key Takeaway

For most buyers, the salary needed for a 500k mortgage in the UK usually sits around £90,000 to £120,000. That range depends on how much deposit you have and how generous the lender is.

Quick answer: To buy a £500k house in the UK, most buyers need a household income between £90,000 and £120,000, depending on the deposit size and lender criteria.

What This Means in Real Life

If you have:

- A small deposit, you will need a higher salary

- With a larger deposit, you may get away with a lower salary

- Other debts, you may need more income than expected

So the real number is not fixed. It changes from one buyer to another.

Monthly Mortgage Repayments on a £500k House

Salary is only one part of the story. You also need to consider the monthly mortgage repayment, as it affects your day-to-day budget.

Estimated Monthly Payments

Here is a rough idea of what repayments might look like.

Mortgage AmountInterest Rate25 Years35 Years

£450,000 4% £2,375 £1,992

£450,000 5% £2,630 £2,272

£400,000 4% £2,111 £1,771

These are only estimates, but they show how much the term and rate matter.

Factors Affecting Monthly Payments

Your monthly cost depends on several things:

- Interest rates

- Fixed vs variable mortgage type

- Mortgage term

- Deposit size

If you borrow less, your payments usually drop. If you choose a longer mortgage term, your monthly payments may also be lower, though you may pay more interest over time.

Why Interest Rates Matter More Than Many Buyers Realize

Even a small rate increase can make a big difference. A 1% increase in interest rate can add hundreds of pounds to your monthly payment.

That is why many buyers prefer a fixed-rate mortgage. It gives more certainty and makes budgeting easier. When rates change, your payments can shift, especially on variable-rate deals.

Can a Single Person Buy a £500k House in the UK?

Yes, a single person can buy a £500k modern house, but it is usually harder to do so. A solo buyer needs to cover the full borrowing capacity on one income, which often means a strong salary and a solid deposit.

Income Requirements for Solo Buyers

As a single buyer, you will often need:

- £100,000+ salary

- Large deposit

- Strong credit score

If you have less than that, you may still qualify, but only if your lender is comfortable with your full financial profile.

Professions More Likely to Qualify

Some jobs give borrowers a better chance because they usually come with higher income or stronger future earnings. These may include:

- Doctors

- Lawyers

- Tech professionals

- Finance executives

That said, your profession alone does not guarantee approval. Lenders still check the full picture.

Alternative Routes for Solo Buyers

If buying alone feels out of reach, you could consider:

- Shared ownership

- Guarantor mortgages

- Longer mortgage terms

These options do not work for everyone, but they may help reduce the gap between what you need and what you can borrow.

Buying a £500k House as a Couple

For many buyers, the easier route is a joint mortgage. When two incomes are combined, affordability often improves a lot.

Combined Income Examples

Buyer 1 SalaryBuyer 2 SalaryCombined Income

£50k £50k £100k

£60k £40k £100k

£70k £30k £100k

A combined income of £100k can often support a £500k purchase, especially with a decent deposit.

Benefits of Joint Applications

A joint application can help because it gives you:

- Higher borrowing power

- Better lender options

- Shared costs

It also means you may have more flexibility with deposit size and monthly repayments.

Potential Downsides

The main downside is that both people are legally responsible for the mortgage. If one person loses income or has credit issues, the application can be affected.

So while joint buying can make things easier, it also means shared liability.

Other Costs of Buying a £500k Property in the UK

Many buyers focus only on the purchase price. But the true cost of buying a home is higher than that.

Stamp Duty Costs

Stamp duty can add a significant extra expense, depending on your situation. The amount varies based on whether you are a first-time buyer, moving home, or buying an additional property.

For a £500k home, stamp duty can be a major cost, so it is important to budget for it early.

Legal and Conveyancing Fees

You will also need to pay for legal work. Typical conveyancing and solicitor costs are usually around:

- £1,000 to £2,500

The exact amount depends on the property and the purchase’s complexity.

Survey and Valuation Costs

A mortgage lender may ask for a valuation, but many buyers also choose a survey for peace of mind.

Common options include:

- Homebuyer survey

- Building survey

These help you spot problems before you commit.

Moving and Furnishing Expenses

Do not forget the practical costs:

- Removal services

- Furniture

- Curtains, appliances, and fittings

- Renovation budget

Even a new home often needs a few changes before it feels right.

Emergency Savings

It is smart to keep savings after you buy. Lenders may approve you, but that does not mean your monthly life will be comfortable.

A healthy cash cushion helps with repairs, bills, and sudden changes in income.

How to Improve Your Mortgage Affordability

If your numbers are close but not quite there, there are several ways to improve your chances.

Increase Your Deposit

A bigger deposit is one of the simplest ways to help.

It can:

- Lower your loan-to-value ratio

- Improve mortgage rates

- Reduce monthly repayments

Even moving from a 10% deposit to a 15% or 20% deposit can make a noticeable difference.

Improve Your Credit Score

Lenders like stability. A stronger credit history can help you borrow more easily.

Try to:

- Pay bills on time

- Reduce credit card use

- Register on the electoral roll

Small improvements can make a real difference over time.

Reduce Existing Debts

Debt affects affordability more than many buyers expect. If you have car finance, credit cards, or personal loans, lenders may reduce how much they are willing to offer.

Paying down these debts before applying can improve your position.

Extend Mortgage Term

A longer mortgage term, such as 30 to 40 years, may reduce monthly repayments.

The upside is lower monthly pressure. The downside is that you may pay more interest overall. So this can help with affordability, but it is not always the cheapest long-term option.

Consider Specialist Lenders

Some buyers do better with specialist lenders, especially if they are:

- Self-employed

- Contractors

- High-income professionals

These lenders may assess income differently and could offer more flexible terms.

Best Areas in the UK Where £500k Buys More Property

A £500k luxury house means very different things depending on where you buy.

London vs Regional Cities

In London, £500k might only buy a flat or a smaller property in many areas. In other parts of the UK, you can buy a much larger home.

Here is the broad contrast:

- London: Often a flat or compact home

- Manchester: A strong family home in many areas

- Birmingham: More space and better value than London

- Leeds: Good-sized homes in many neighborhoods

- Newcastle: £500k can go much further

What £500k Gets You Across the UK

In broad terms, £500k may buy:

- A flat in London

- A detached or semi-detached house in the North of England

- A larger family home in parts of Wales

So location changes the meaning of your budget completely.

Lifestyle vs Commuting Trade-Offs

Some buyers choose cheaper areas and commute. Others work remotely and can live farther from city centers.

This is where lifestyle matters. Ask yourself:

- Do you need to be near work?

- Would you accept a longer commute?

- Is more space more important than location?

These answers can shape your decision as much as salary does.

Common Mistakes Buyers Make When Budgeting for a £500k House

A £500k purchase is exciting, but it is easy to make avoidable mistakes.

Focusing Only on Mortgage Approval

Some buyers think approval means affordability. It does not.

Just because a lender says yes does not mean the monthly costs will feel comfortable. Always think about your real-life budget.

Underestimating Monthly Costs

Your mortgage is only one expense. You also need to budget for:

- Utilities

- Insurance

- Council tax

- Maintenance

These costs can add up quickly.

Draining Savings for the Deposit

It may feel good to put down a big deposit, but do not leave yourself with nothing. You still need emergency savings after completion.

Ignoring Future Interest Rate Changes

If you choose a variable rate, your payments may rise later. Even fixed-rate deals eventually end, so always plan for what happens next.

Frequently Asked Questions

How much do I need to earn to buy a £500k house in the UK?

Most buyers need a household income of around £90,000-£120,000. The exact amount depends on the deposit, debts, and lender rules.

Can I buy a £500k house with a £50k deposit?

Yes, but it may be tight. A £50k deposit means borrowing £450,000, so you will usually need around £100,000 income or more, depending on the lender.

What mortgage can I get on a £60k salary?

A rough estimate is around £240,000 to £270,000, depending on the lender and your financial situation. If you have no debts and a strong profile, you may be able to borrow a bit more.

Can first-time buyers afford a £500k property?

Some can, especially with a high income or help with a deposit. But for many first-time buyers, £500k is difficult to afford without a strong salary or a joint application.

How much are repayments on a £500k mortgage?

If you borrow around £450,000, repayments may be roughly £2,000 to £2,600 per month, depending on interest rate and term.

Is a £100k salary enough for a £500k house?

It can be, but it depends on your deposit and debts. A £100k salary with a solid deposit may work well. Without much deposit, it becomes harder.

| Income multiple lender uses | Approx. salary needed for £500k house | Notes |

|---|---|---|

| 3× income | £166,667 | Lower multiple; stricter lending; higher income needed. |

| 3.5× income | £142,857 | Conservative affordability check. |

| 4× income | £125,000 | Common “mid‑range” requirement. |

| 4.5× income | £111,111 | Typical norm; many lenders use ~4–4.5× salary. |

| 5× income | £100,000 | Higher‑income case; some lenders allow up to 5× earnings. |