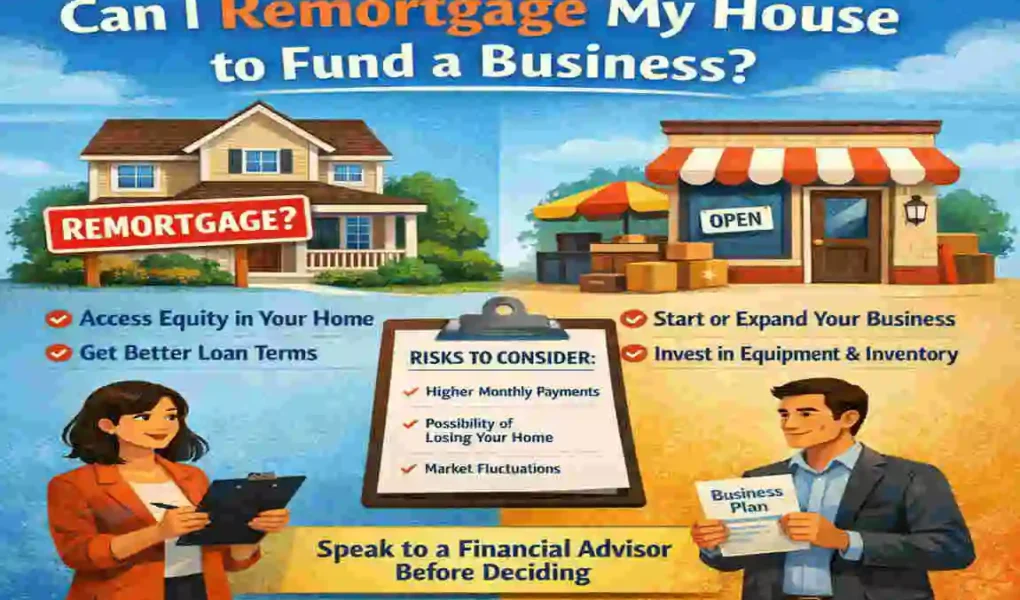

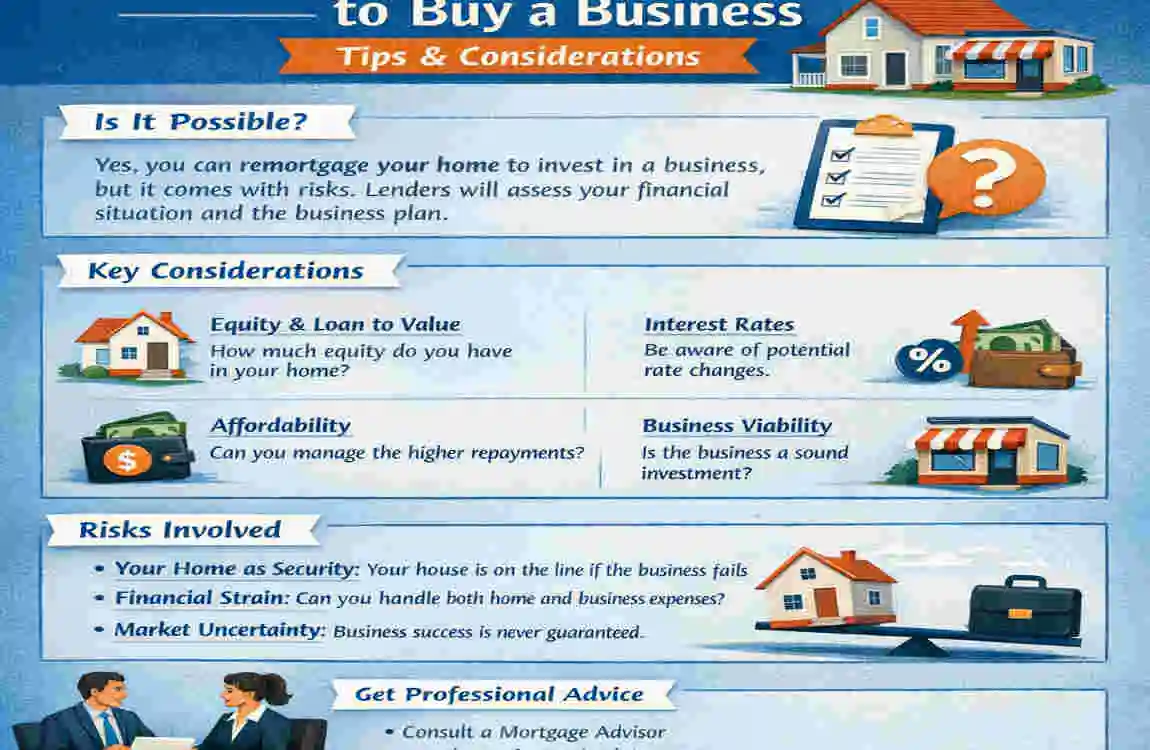

If you are asking, “Can I remortgage my house to buy a business?” you are probably looking for a practical way to raise money without giving up control of your idea. That is a common thought for many people who want to start a company or buy an existing one.

A remortgage can unlock the value tied up in your home. In simple terms, this means you borrow against the equity you have built over time. Some people use this money to expand a business, cover startup costs, or buy an established business that already makes money.

This can be a useful route, but it is also a serious decision. Your home is on the line, and the business itself may not succeed. So before you move forward, you need to understand how remortgage for business funding works, what lenders want, the risks involved, the costs, and the safer alternatives.

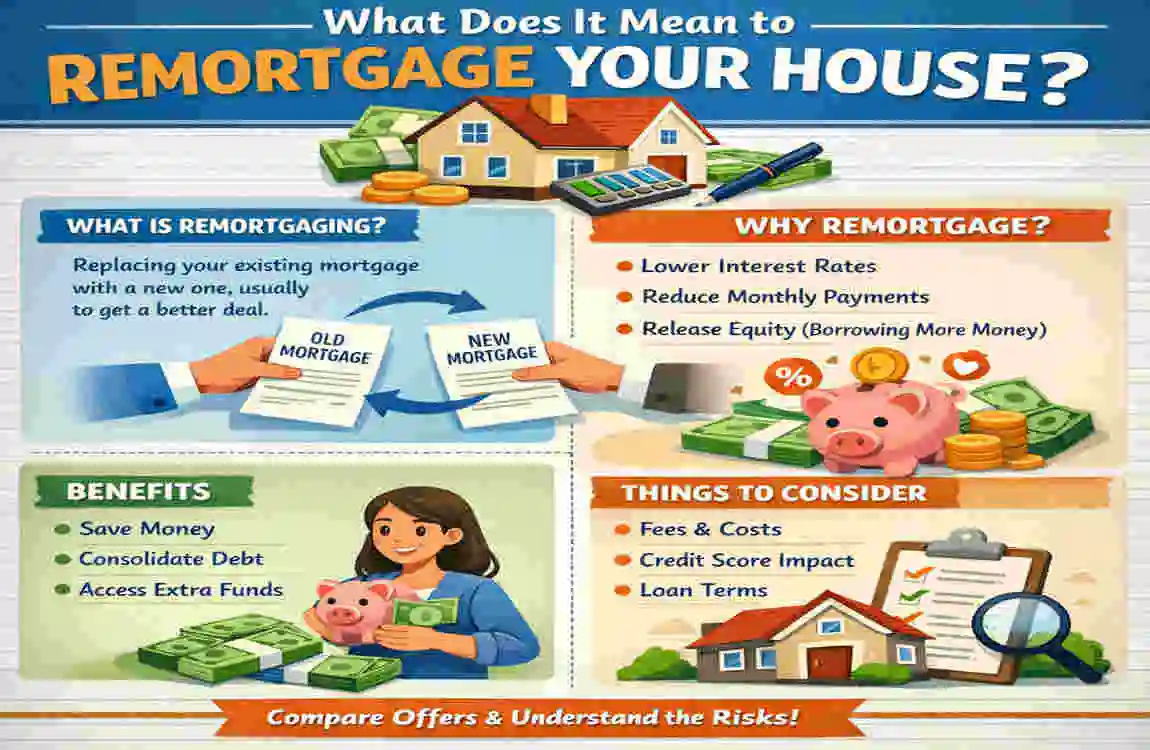

What Does It Mean to Remortgage Your House?

Definition of Remortgaging

A remortgage means replacing your current mortgage with a new one, usually with a different lender or a new deal from the same lender. People often do this to get a better rate, change the loan term, or borrow more money.

This is different from a second mortgage. A second mortgage is an additional loan secured by the same property while your first mortgage remains in place. A remortgage usually combines all the existing loans into a single new mortgage.

How Home Equity Works

Home equity is the part of the home you truly own. It is the difference between your luxury home‘s current market value and how much you still owe on the mortgage.

For example, if your home is worth $300,000 and you still owe $180,000, your equity is $120,000. Lenders may let you borrow a portion of that equity, depending on your income, credit, and the property value.

Why People Use Remortgages for Business Funding

People often use a remortgage to start or grow a business because it can provide a larger amount than many personal loans. Common uses include:

- Buying an existing business

- Funding a startup

- Expanding operations

- Renovating commercial space

- Paying off expensive debts before launching

This can be attractive because the rates are often lower than unsecured borrowing. Still, lower cost does not mean lower risk.

Can I Remortgage My House to Buy a Business?

The Simple Answer

Yes, in many cases, you can remortgage your house to buy a business. But approval is not automatic. Lenders will look closely at your finances, your property, and how you plan to use the money.

Some lenders are happy to release funds for business use. Others may be more cautious if the borrowing is linked to a startup or a risky business idea.

What Lenders Look For

When reviewing a remortgage business loan, lenders usually want to see:

- Credit score — a strong credit history helps your chances

- Income stability — steady pay or reliable self-employed income

- Existing debts — too much debt can reduce approval odds

- Property value — the luxury home must have enough equity

- Business plan — especially if the money will fund a new business

They want to know that you can handle the new mortgage payments even if the business takes time to grow.

Residential vs Commercial Lending

A residential mortgage is tied to your home, while commercial lending is tied to a business or business property. If you use your home to fund a business, the lender is still making a residential lending decision. Still, they may care about the business purpose.

That matters because some lenders do not like business-related borrowing if the purpose feels too uncertain. A stable purchase of an existing business is often seen as safer than funding a brand-new startup.

Common Reasons Applications Are Rejected

Your application may be declined if you have:

- Poor credit history

- Not enough home equity

- High debt-to-income ratio

- Unstable earnings

- A weak or unrealistic business plan

If any of these apply, you may want to improve your finances before applying.

Advantages of Remortgaging to Fund a Business

Lower Interest Rates

One of the biggest benefits of using home equity to buy a business is that mortgage rates are often lower than business credit cards or unsecured loans. That can reduce borrowing costs over time.

Access to Larger Amounts

A remortgage can unlock a larger sum than many other funding options. This can be useful if you need substantial funds to buy equipment, pay suppliers, or acquire an existing company.

Flexible Repayment Terms

Mortgage terms are usually longer than personal loans. That means the monthly payments can be more manageable, which may help you protect cash flow in the early stages of the business.

Potential Business Growth Opportunities

If you choose the right business, this money can help you build something valuable. Buying an established business or investing in expansion may give you a better chance of success than starting from zero.

Risks of Using Your Home to Buy a Business

Your Home Is at Risk

This is the biggest concern. If you cannot keep up with mortgage payments, you could lose your modern home. That is why this decision should never be made lightly.

Increased Long-Term Debt

A remortgage may feel manageable month to month, but over time, you may end up paying more interest. Even if the payment is lower, the overall debt can stay with you for many years.

Business Failure Concerns

Not every business succeeds. Startups are especially risky, and even existing businesses can run into trouble. If the business fails, you still owe the mortgage.

Emotional and Financial Stress

Borrowing against your luxury home can create pressure for you and your family. If business income is slow or uncertain, stress can build quickly.

Property Market Risks

If house prices fall, your equity can shrink. That can affect your borrowing position and make it harder to refinance later.

How Much Can You Borrow Through a Remortgage?

Loan-to-Value Ratio (LTV)

Lenders often use the loan-to-value ratio (LTV) to determine how much they will lend. This is the percentage of the property value they are willing to finance.

For example, if your home is worth $250,000 and the lender allows an 80% LTV, the total mortgage could be up to $200,000. If you already owe $140,000, you may be able to release some of the remaining equity.

Factors Affecting Borrowing Limits

Your borrowing limit depends on:

- Your income

- Your home’s current value

- Your credit profile

- Your repayment history

- Your current mortgage balance

Lenders want to ensure the new loan remains affordable, even if your business takes time to generate income.

Example Borrowing Scenario

Let’s say your home is worth $400,000 and your current mortgage balance is $220,000. If a lender is willing to lend up to 75% LTV, the maximum mortgage might be $300,000. That means you may be able to release up to $80,000 in equity, minus fees and costs.

Steps to Remortgage Your House for Business Funding

Calculate Your Home Equity

Start by checking your luxury home‘s current value and subtracting what you owe. This gives you a rough idea of how much equity may be available.

Review Your Credit Score

Before applying, look at your credit report. If there are errors or unpaid debts, fix them first. A stronger credit score can improve your chances.

Prepare a Business plan

If you are using the money for a business, a clear plan matters. Show how the business will make money, what the costs are, and how you plan to repay the mortgage.

Compare Mortgage Lenders

Not all lenders treat business-related borrowing the same way. Compare options carefully and ask whether they allow business use of funds.

Submit Documentation

You will usually need proof of income, bank statements, property details, ID, and maybe business documents. Keep everything organized to avoid delays.

Receive Funds and Invest Carefully

Once approved, use the money wisely. Do not spend it too quickly. Focus on the most important business expenses first.

Quick checklist before applying

- Check your equity

- Review your credit

- Test your business idea

- Compare lenders

- Think about worst-case scenarios

Alternatives to Remortgaging Your House

Business Loans

A business loan may be a better fit if you want to keep your dearm home separate from your company. The interest may be higher, but your house is not directly at risk in the same way.

SBA or Government Programs

Depending on where you live, there may be public funding programs for small businesses. These can offer better terms or support for startup owners.

Business Investors

If you are open to giving up some control, investors may provide funding in exchange for a share of the business. This can reduce pressure on your personal finances.

Personal Loans

A personal loan may be easier to arrange than a remortgage. Still, the amounts are often smaller, and rates can be higher.

Crowdfunding

If your business idea is appealing to the public, crowdfunding may help you raise capital without using your home as collateral.

Tips Before You Remortgage Your Home for a Business

Speak With a Financial Advisor

A professional can help you check whether the numbers make sense. This is especially important if you are using your luxury home for a startup.

Avoid Borrowing More Than Needed

It can be tempting to take extra cash “just in case.” Try to borrow only what you truly need.

Build an Emergency Fund

If possible, set aside some savings for mortgage payments and unexpected business costs.

Stress-Test Your Business plan

Ask yourself what happens if sales are slow, costs rise, or the business takes longer to grow.

Compare Multiple Mortgage Offers

Do not accept the first offer you see. Even a small change in interest rate can make a big difference over time.

Real-Life Example Scenario

Imagine a homeowner with a property worth $350,000 and an existing mortgage of $180,000. They remortgage and release $60,000 in equity to buy a small café.

Their new monthly payment rises by about $250, but they believe the café can produce a steady income within six months. In the first year, the business performs well enough to cover costs and generate profit.

This is a realistic example of how home equity for business purchase can work when the business is solid, and the borrowing amount is sensible. But if sales had dropped, the homeowner would still be responsible for the mortgage.

Frequently Asked Questions

Can I remortgage my house to buy a business with bad credit?

It is harder, but not always impossible. Some lenders may still consider you if you have strong equity or a stable income. Still, bad credit can reduce your options and increase costs.

Is remortgaging cheaper than a business loan?

Often, yes. Mortgage rates are usually lower than business loan rates. But the real cost depends on fees, term length, and how long you keep the loan.

How long does a remortgage process take?

It can take a few weeks to a couple of months. The timeline depends on the lender, paperwork, property checks, and how quickly you respond.

Can self-employed people remortgage their homes?

Yes, self-employed borrowers can remortgage. Lenders may request tax returns, bank statements, and other financial records to verify income.

What happens if my business fails?

You still owe the mortgage. If payments become unmanageable, your home may be at risk. That is why this type of borrowing needs careful planning.

Do lenders ask why I need the money?

Yes, many do. They may want to know whether the funds are for a business purchase, expansion, or another purpose.

Can I use remortgage funds for a startup business?

Yes, but startups are riskier. Lenders may be stricter because new businesses have no track record.

Are there tax benefits to remortgaging for business purposes?

Sometimes there may be tax implications, but this depends on your location and business structure. It is best to ask a tax professional before you decide.

| Topic | Details |

|---|---|

| Main Question | Can I remortgage my house to buy a business? Yes, many homeowners use home equity to fund a business purchase or startup. |

| What Is Remortgaging? | Remortgaging means replacing your current mortgage with a new one to release equity from your home. |

| How It Helps Fund a Business | You can use the released cash to buy an existing business, invest in a startup, expand operations, or cover business expenses. |

| Eligibility Requirements | Lenders usually check your credit score, income, home equity, property value, and debt-to-income ratio. |

| Typical Borrowing Amount | Most lenders allow borrowing based on your available home equity and Loan-to-Value (LTV) ratio. |

| Main Benefits | Lower interest rates, larger borrowing amounts, and longer repayment terms compared to some business loans. |

| Main Risks | Your home could be at risk if you fail to make mortgage repayments. Business failure may also create financial stress. |

| Documents Needed | Proof of income, mortgage statements, bank records, identification, and sometimes a business plan. |

| Alternative Funding Options | Business loans, investors, personal loans, crowdfunding, and business credit lines. |

| Best For | Homeowners with strong equity, stable income, and a well-planned business opportunity. |

| Not Ideal For | People with unstable income, poor credit, or high-risk business ideas. |

| Expert Tip | Always compare lenders and speak with a financial advisor before remortgaging your home for business funding. |

| SEO Focus Keyword | can i remortgage my house to buy a business |