It is the middle of the night, and a massive storm rolls through your neighborhood. The wind is howling, heavy rain is lashing against your windows, and you can hear the unmistakable sound of hail pounding on your house. When you wake up the next morning and step outside with your cup of coffee, your heart sinks. You see broken shingles scattered across your front lawn, a dented gutter, and a suspicious water stain forming on your living room ceiling. Panic starts to set in. What do you do next?

Roofs are the first line of defense for your home. Because they take the brunt of extreme weather, they are one of the most common reasons homeowners reach out to their insurance providers. From severe hail and wind damage to unexpected tree falls and sudden leaks, roof issues are incredibly frequent. In fact, weather-related events make up a massive portion of property claims every single year.

What Triggers a Roof Insurance Claim?

Before you pick up the phone to call your insurance agent, you need to understand what actually qualifies for a claim. Not every missing shingle or minor leak means your insurance company will write you a check. Understanding these triggers helps immensely when you are getting ready to file a roof damage claim.

Insurance policies are generally designed to protect you from sudden, accidental, and unavoidable events. They are not maintenance plans. If your roof is simply old and worn out, your insurance provider will likely expect you to pay for the replacement out of your own pocket.

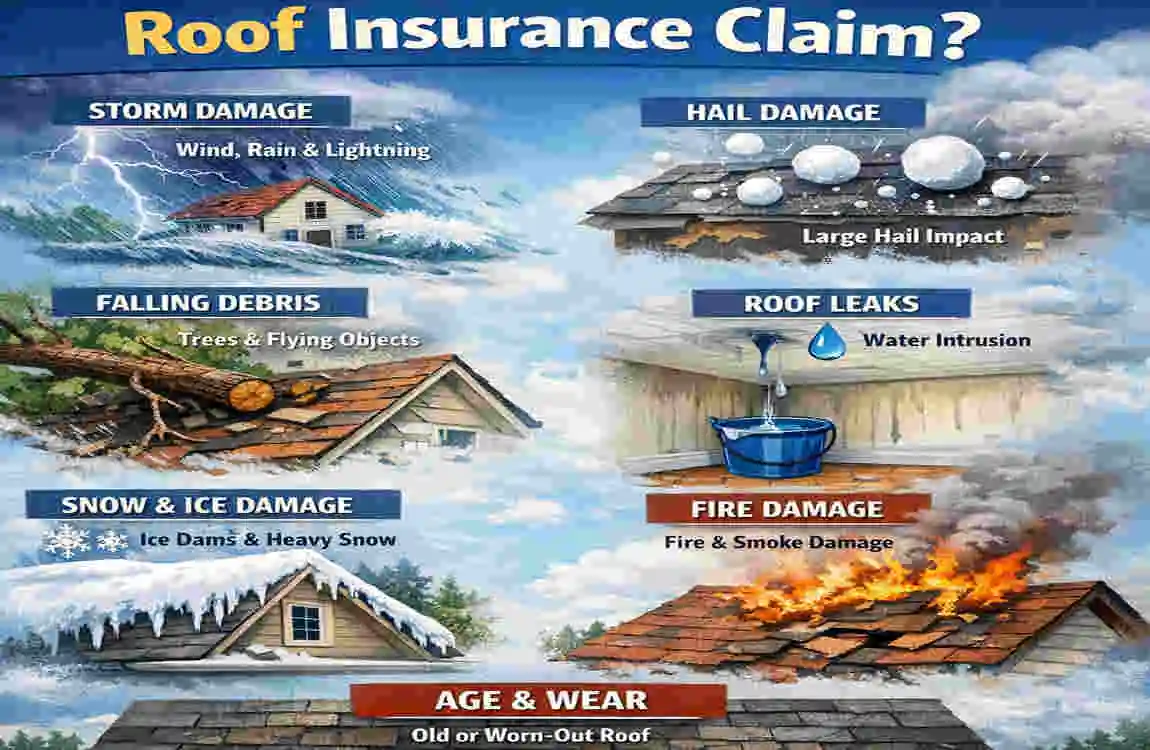

Common Covered Causes (Sudden Perils)

Most standard homeowners’ insurance policies cover damages caused by sudden, unexpected events. These are often referred to as “perils.”

- Severe Storms: This includes high winds that rip shingles completely off your roof, or hail that bruises and cracks your roofing materials.

- Fallen Trees or Branches: If a healthy tree suddenly snaps during a storm and crashes through your attic, this is typically a covered event.

- Fire and Smoke: Whether it is a house fire or a wildfire that spreads to your property, fire damage to your roof is almost always covered.

- Vandalism: If someone intentionally damages your roof, your policy will usually help cover the repairs.

Common Exclusions (What Is Not Covered)

On the flip side, insurance companies have strict rules about what they will not pay for.

- Normal Wear and Tear: If your roof is 25 years old, curling at the edges, and simply deteriorating from age, insurance will not cover a new one.

- Neglect and Lack of Maintenance: If a small, easily fixable leak was ignored for years and eventually led to the rotting of your entire roof deck, the insurance company will likely deny the claim due to negligence.

- Pest Damage: Damage caused by squirrels, raccoons, or birds nesting in your roof is usually excluded.

- Floods: Standard policies cover water from above (such as rain through a storm-created hole). Water rising from the ground requires a completely separate flood insurance policy.

Covered vs. Excluded Roof Damages

To make this easier to digest, here is a simple breakdown of what is usually covered and what is not.

Damage Type Covered? Example Scenario

Hail or Wind Yes High winds tear off shingles, or hail causes deep dents.

Wear & Tear No Shingles become brittle and crack due to decades of sun exposure.

Tree Fall Yes (usually) A sudden gust of wind knocks a heavy branch onto your roof.

Pest Infestation : No Raccoons tear a hole through your shingles to build a nest in your attic.

Fire Damage Yes , an accidental fire damages the structural supports of your roof.

Types of Roof Insurance Coverage

To fully grasp how an insurance claim on a roof works, you need to understand the specific type of coverage you actually have. Not all policies are created equal. When you look at your paperwork, the payout you receive will largely depend on two main valuation methods, as well as your deductible.

Let’s break these down into simple terms, so you know exactly what to expect when it is time to get paid.

Actual Cash Value (ACV) vs. Replacement Cost Value (RCV)

These are the two ways your insurance company will calculate how much to pay for your damaged roof.

Actual Cash Value (ACV) means the insurance company pays you what your roof is worth today, taking into account its age and condition. Think of it like a used car. If you total a ten-year-old car, the insurance company doesn’t buy you a brand-new one; they pay you the car’s cash value. If your roof is 15 years old and gets destroyed by hail, an ACV policy will deduct 15 years of depreciation from your payout. This means you will likely have to pay a significant out-of-pocket cost to afford a brand-new roof.

Replacement Cost Value (RCV) is the better, more comprehensive option. With an RCV policy, the insurance company pays to replace your damaged roof with a brand-new roof of similar quality, without subtracting money for its age. While RCV policies usually have slightly higher monthly premiums, they save you a massive amount of money and stress when a disaster strikes.

Understanding Your Deductible

Your deductible is the amount of money you are required to pay out of your own pocket before your insurance coverage kicks in.

For example, if your roof repairs cost $10,000 and your deductible is $1,000, the insurance company will write you a check for $9,000. You must pay the remaining $1,000 to your roofing contractor.

Pay close attention to your policy details, especially if you live in an area prone to severe weather. Some policies have a flat-rate deductible (like $1,000 or $2,000). In contrast, others have a percentage-based deductible specifically for wind and hail damage. A percentage deductible is usually 1% to 5% of your home’s total insured value. If your home is insured for $300,000 and you have a 2% wind/hail deductible, you will be responsible for paying $6,000 out of pocket before your insurance kicks in.

Extended and Additional Coverages

Sometimes a damaged roof leads to other, more expensive problems. Check your policy for extended coverage. For instance, if a tree falls on your roof and rainwater ruins your living room’s drywall and hardwood floors, your policy should cover that interior damage too. Additionally, if the damage is so severe that you cannot safely live in your house during repairs, “Loss of Use” coverage can help pay for a hotel stay and meals.

Knowing your specific policy details is the absolute key to making the roof insurance claim process work smoothly for you.

Step-by-Step Guide: How Does an Insurance Claim on a Roof Work?

Now we reach the most critical part of our guide. When a storm passes, and you are left with a broken roof, the steps you take next will dictate how successful your claim will be.

Here is your ultimate, easy-to-follow, step-by-step breakdown.

Assess the Damage Safely (Day 1)

Your priority after a storm is safety. Do not climb up onto a slippery, damaged roof yourself. Leave the climbing to the trained professionals. Instead, you want to safely assess and document the damage from the ground.

Grab your smartphone or a camera and start walking around your property. You are looking to build a visual timeline of the destruction.

- Take wide-angle photos of your entire house.

- Zoom in on areas where you can visibly see missing shingles, dented metal flashing, or sagging spots.

- Take photos of the ground. Are there broken shingles in your grass? Take a picture.

- Check your gutters and downspouts for hail damage.

- Walk inside your house and check the ceilings on your top floor and attic for any fresh water stains or active drips.

Immediate Temporary Fixes: If water is actively leaking into your home, you are responsible for preventing further damage. This is called “mitigating your loss.” You can hire a local roofer or handyman to place a temporary waterproof tarp over the hole. Always save the receipt for this emergency service. Your insurance company will almost always reimburse you for temporary emergency repairs designed to protect your home.

Review Your Insurance Policy

Before you call your insurance agent, take a deep breath, sit down, and find your insurance documents. You are looking for a document called the Declarations Page. This is usually the first few pages of your policy that summarize your coverage.

You want to find the answers to three specific questions:

- Is my coverage Actual Cash Value (ACV) or Replacement Cost Value (RCV)?

- What is my exact deductible amount for wind or hail damage?

- Are there any specific exclusions I need to be aware of?

Knowing these facts beforehand empowers you. When you speak to the insurance representative, you will sound informed and prepared, which sets a great tone for the rest of the process.

File the Initial Claim

Do not procrastinate on this step. Insurance policies usually require you to report damage promptly, typically within 24 to 72 hours after a severe weather event.

Call your insurance agent or dial your provider’s 24/7 claims hotline. Alternatively, many modern insurance companies allow you to file a claim directly through their smartphone app or website.

When you file, keep it simple and stick to the facts. Provide your policy number, the date and time the storm happened, and a brief description of the damage you can see from the ground. Let them know if you have already applied a temporary tarp. By the end of this conversation, the representative should give you a Claim Number. Write this number down and keep it safe—you will need it for every future conversation regarding your roof.

Schedule the Adjuster Inspection

Once your claim is officially in the system, the insurance company will assign an insurance adjuster to your case. The adjuster’s job is to visit your home, inspect the roof, verify that the damage was caused by a covered event, and estimate the cost of repairs.

Depending on how many other homes in your area were damaged by the same storm, it might take anywhere from a few days to two weeks for the adjuster to arrive.

Pro Tip for Homeowners: The insurance adjuster works for the insurance company, not for you. Their goal is to manage the company’s expenses. It is highly recommended that you hire your own trusted, independent, and licensed roofing contractor to be present at your home during the adjuster’s inspection. Your roofer can point out hidden damages that the adjuster might accidentally overlook, ensuring you get a fair and thorough evaluation.

Get Repair Estimates

Do not simply accept the insurance adjuster’s initial repair estimate without doing your own homework. The adjuster’s estimate is often based on regional averages and software calculations, which might not reflect the actual cost of labor and high-quality materials in your specific neighborhood.

Reach out to two or three reputable, locally licensed, and insured roofing contractors. Ask them to provide you with a detailed, itemized quote for repairing or replacing your roof.

If your trusted roofer’s estimate is higher than the insurance adjuster’s estimate, do not panic. This is completely normal. Your roofer will simply send their detailed estimate to the insurance company to negotiate the difference. They use the same technical language and can usually reach agreement on the final price.

Review and Approve the Settlement

Once the insurance company and your roofer agree on the scope of work and the price, the insurance company will finalize your settlement. You will receive a document breaking down exactly what they are paying for, line by line.

If you have a Replacement Cost Value (RCV) policy, it is important to understand how the payout is calculated. Usually, you do not get one giant check upfront.

- Check 1 (The ACV Check): The insurance company will send you an initial check for the roof’s Actual Cash Value (the value minus depreciation and your deductible). You use this money to buy materials and get the contractor started.

- Check 2 (The Depreciation Check): Once the roofing job is finished, you send the final invoice to the insurance company. They will then issue a second check covering the depreciation amount they had withheld. This ensures that you actually completed the work.

Hire a Contractor and Complete Repairs

With the settlement approved and the initial funds in your bank account, it is time to officially hire your roofer and schedule the work.

Always verify your contractor. Make sure they have a valid physical address in your city, active licenses, and proof of liability and workers’ compensation insurance. Be very wary of “storm chasers”—roofers who travel from out of state, knock on your door after a storm, demand cash upfront, and do shoddy work before disappearing.

Once you choose a reliable local contractor, they will tear off the old damaged materials, inspect the underlying wood deck for hidden rot, and install your brand-new roof.

Close the Claim

You are almost at the finish line! Once the contractor sweeps up the last stray nail from your driveway and you are happy with the new roof, they will hand you a final invoice.

Submit this final invoice, along with photos of the beautifully completed new roof, to your insurance adjuster. This serves as proof of completion. The insurance company will then release any final withheld funds (the depreciation check we mentioned earlier), allowing you to pay your contractor their final balance. Once that is done, your claim is officially closed.

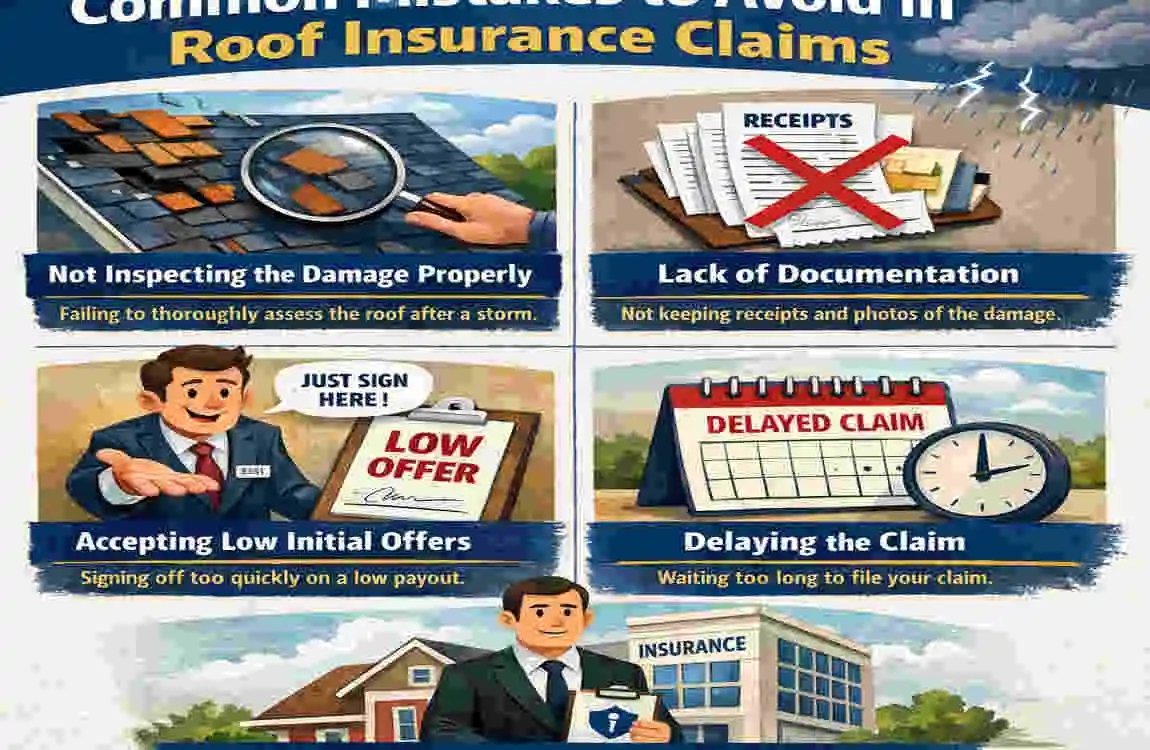

Common Mistakes to Avoid in Roof Insurance Claims

Even when you know the steps, the roof insurance claim process can be tricky. Homeowners often make simple mistakes that cost them thousands of dollars or result in their claims being completely denied.

Avoid these common pitfalls to ensure your process goes smoothly:

- Delaying the Report: Time is not your friend after a storm. If you wait weeks or months to report a damaged roof, the insurance company might argue that the damage resulted from neglect rather than the storm. Report the damage immediately.

- Skipping the Documentation Phase: Without photos and videos of the damage right after it happened, it becomes your word against the insurance company. Always take clear, timestamped photos of the damage, the temporary repairs, and the debris in your yard.

- Accepting Lowball Offers Immediately: The first check the insurance company offers you is not always their final offer. If your independent roofer proves that the repairs will cost more than the adjuster estimated, you have the right to ask the insurance company to supplement the claim. Never feel pressured to accept a payout that won’t cover quality repairs.

- Not Reading the Fine Print: Being surprised by a massive percentage-based deductible after a hail storm is a terrible feeling. Always read your policy documents so you understand exactly what your financial responsibilities are.

- Doing DIY Repairs Without Approval: While putting a temporary tarp over a leak is encouraged, do not attempt to permanently patch shingles or replace roof sections yourself before the adjuster sees the damage. If you alter the scene too much, the adjuster cannot properly assess the original storm damage, and your claim could be denied.

How Long Does a Roof Claim Take?

When you are living with a tarp on your roof, every day feels like a week. It is completely natural to wonder how long this entire ordeal will last.

The timeline can vary wildly based on your location and the severity of the weather event. If a massive hurricane hits your state, adjusters will be backlogged for weeks. If it were just an isolated thunderstorm in your neighborhood, the process would be much faster.

Here is a general timeline of what you can expect under normal circumstances:

Claim Step: Typical Time Frame

Filing the Claim 1 to 2 days

Adjuster Inspection 1 to 2 weeks

Getting Contractor Estimates in 3 to 7 days

Review & Settlement Payout 2 to 4 weeks

Roof Replacement Work 1 to 3 days (once scheduled)

Remember, supply chain issues for roofing materials or disputes over the settlement amount can easily extend this timeline. Patience, paired with polite but persistent follow-ups with your insurance agent, is the best approach.

FAQs: Roof Insurance Claims

We know that even with a detailed guide, you probably still have some specific questions bouncing around in your head. Let’s tackle some of the most frequently asked homeowner questions about the process.

How does an insurance claim on a roof work if it’s only partial damage?

Insurance companies prefer the most cost-effective solution. If a storm only tore off a small section of shingles on one side of your house, and the rest of the roof is perfectly healthy, the insurance company will likely only pay to patch and repair that specific damaged section. They will try to find matching shingles. However, if your roof is older and matching shingles are no longer manufactured, you might have grounds to argue for a full replacement, as a severely mismatched roof impacts your home’s value.

Does insurance cover a full roof replacement?

Yes, but only if the damage is severe enough or widespread enough to justify it. If a massive hailstorm destroys the integrity of the shingles across the entire roof surface, a full replacement is warranted. Additionally, if the cost of repairing multiple sections of the roof exceeds the cost of replacing the entire roof, the insurance company will opt for a full replacement.

What if the insurance adjuster undervalues my roof damage?

You do not have to just accept a low valuation. This is why having your own roofing contractor is so important. Your contractor can write a detailed “supplemental claim” with photographic evidence showing that additional funds are needed for materials or labor. If you and the insurance company still cannot agree, you have the right to hire a “Public Adjuster.” A public adjuster is an independent professional who works for you (not the insurance company) to negotiate the best possible settlement. However, they do take a percentage of your final payout as their fee.

Can I choose my own roofer for the repairs?

Absolutely. While your insurance company might offer a list of “preferred contractors” they work with frequently, you are under no legal obligation to use them. It is your home, and you have the right to choose any licensed, bonded, and insured local roofing contractor that you trust.

Will my insurance premiums go up after I file a roof damage claim?

This is a tricky question, and the answer is usually “it depends.” If you file a claim for something preventable, like a slow leak you ignored, your rates might increase because you are seen as a high-risk homeowner. However, if your roof was destroyed by an “Act of God”—like a massive, unpreventable neighborhood hail storm or tornado—insurance companies in many regions are legally prohibited from raising only your individual rates. However, they might raise the rates for everyone in your entire zip code because the area is now deemed prone to extreme weather.