Finding your absolute dream home, putting in an offer, and skipping the entire stressful mortgage application process. No anxious waiting for lender approvals, no worrying about rising interest rates, and no massive stacks of financial paperwork to appease a bank. If you find yourself wondering, “Can you buy a house with cash in the UK?” you are certainly not alone.

In fact, recent data shows that cash buyers are taking over a massive chunk of the property market. Back in 2025, cash buyers made up a staggering 35% of all home purchases in the UK, according to HM Land Registry data. Buying a property outright is not just a pipe dream for the ultra-wealthy; it is a highly popular and practical route to homeownership for many people.

Buying a house with cash means you bypass the bank entirely. You use your own saved funds to purchase the property outright. This fast-tracks your journey, cuts down your timeline from a sluggish six months to a breezy eight to twelve weeks, and gives you incredible negotiating power. Sellers love cash buyers because you represent a sure thing in a market full of uncertainties.

What Does “Buying a House with Cash UK” Really Mean?

When you hear the term “cash buyer,” you might picture someone walking into an estate agent’s office with a silver briefcase full of £50 notes. While that makes for a great movie scene, the reality is much more digital and secure. Let us break down exactly what it means to be a cash buyer in the modern UK property market.

Defining a True Cash Purchase

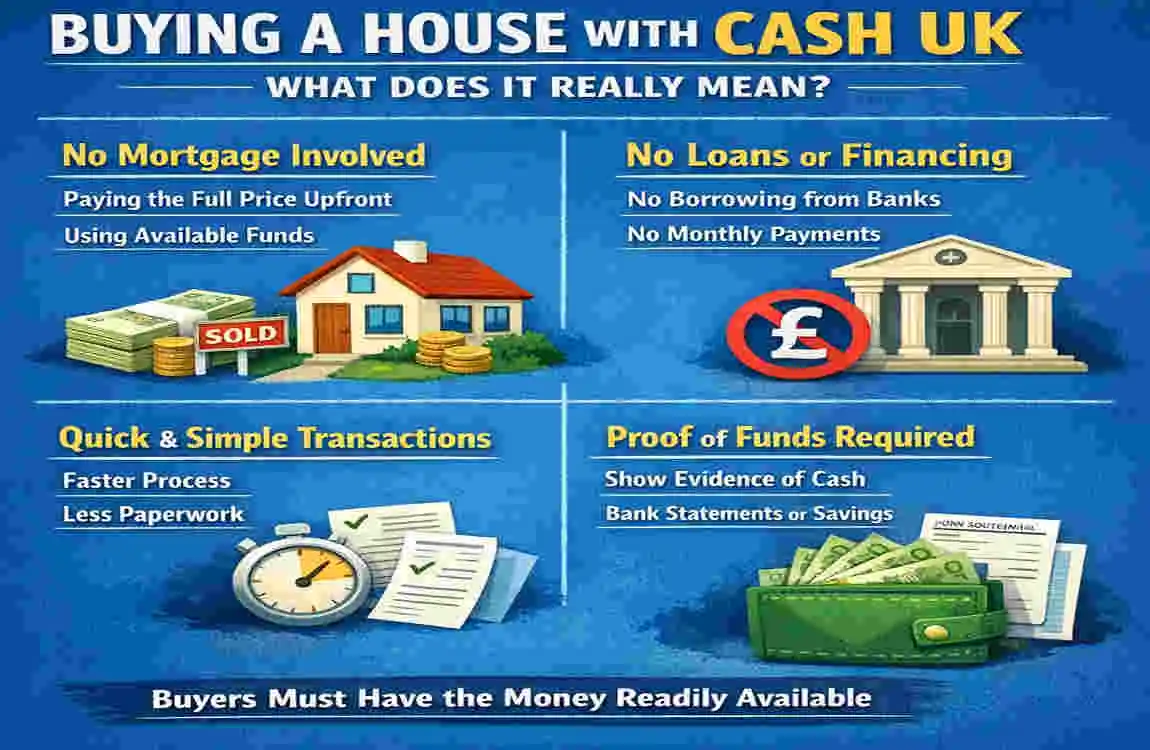

Buying a house with cash means you have the total purchase price of the property sitting in your bank account, ready to transfer. You are making a full payment from your personal savings, your investment dividends, an inheritance, or the proceeds from selling a previous property.

To be classified as a true cash buyer, you cannot rely on any loan to fund the purchase. For example, if you are using an equity release scheme on your current home, or if you need a bridging loan to cover the gap between buying and selling, estate agents will not view you as a pure cash buyer. You must have the liquid funds available right now.

How Cash Buying Differs from Mortgage Purchases

The biggest difference between a cash purchase and a mortgaged purchase is the distinct lack of a lender. When you get a mortgage, the bank has a massive say in your property journey. They send out their own surveyors to ensure the house is worth the money, and they can pull their funding at the very last minute if they find an issue.

When you buy with cash, you answer only to yourself. You do not need lender approval. You do not have to pay expensive mortgage arrangement fees, and you will not spend the next twenty-five years paying thousands of pounds in interest. However, you still have to follow the standard UK property laws, pay your taxes, and hire legal professionals to handle the paperwork.

Who Exactly Qualifies as a Cash Buyer?

You might think only millionaires buy houses with cash, but the demographic is actually incredibly diverse. High-net-worth individuals certainly make up a portion of this group, but they are not the only ones.

Downsizers are very common cash buyers. If you sell a large family home for £600,000 and buy a smaller bungalow for £300,000, you can easily pay cash. Property investors also frequently use cash to snap up auction properties or fix-and-flip opportunities quickly. Finally, expats returning to the UK with savings from lucrative overseas jobs often prefer to buy outright to avoid the strict lending criteria applied to foreign income.

The 2026 Trend: Why Cash Deals Are Surging

You might be asking why cash deals are becoming so prevalent. As we move through 2026, fluctuating interest rates have made mortgages more expensive and unpredictable. Many buyers who have the means are choosing to avoid the banking system altogether. In fact, year-over-year, cash deals have surged as buyers seek the financial peace of mind that comes with owning a home outright from day one.

Pros and Cons of Buying a House with Cash in the UK

Before you dive into emptying your savings account, it is crucial to weigh both sides of the coin. Buying a home outright offers incredible advantages, but it also comes with a few financial drawbacks that you need to consider carefully.

The Amazing Benefits (Pros)

There is a reason estate agents’ eyes light up when you say you are a cash buyer. The benefits are substantial for everyone involved in the transaction.

- Lightning-Fast Completion: When you do not have to wait for a bank to underwrite a mortgage, you save weeks, if not months, of time. Cash purchases often go through 40% quicker than financed deals. If both parties are motivated, you can get your keys in less than a month.

- Stronger Negotiating Power: Sellers want a stress-free sale. Property chains—where a sale depends on someone else buying another house—frequently collapse when a mortgage falls through. As a cash buyer, you break that chain. Because you offer certainty, sellers accept cash offers about 90% of the time, even if you offer slightly below the asking price.

- Zero Mortgage Fees or Interest: This is the big one. Mortgages are expensive. When you buy with cash, you skip the valuation fees, the broker fees, and the arrangement fees. More importantly, you save tens of thousands of pounds in interest payments over what would normally be a 25-year term.

- Simpler Survey Process: Mortgage lenders force you to get specific valuations to protect their investment. While you should absolutely still get a survey (more on this later!), you get to choose the surveyor and the level of detail, putting you firmly in the driver’s seat.

- Total Peace of Mind: You own 100% of your home from the moment you move in. If you lose your job or face financial hardship, nobody can repossess your house for missing a mortgage payment.

The Potential Pitfalls (Cons)

While the pros are incredibly tempting, you must look at the cons to make an informed decision about your financial future.

- Ties Up Your Capital: When you sink all your cash into a house, that money becomes illiquid. You cannot easily access it if an emergency arises or if a brilliant business opportunity presents itself. This is known as an opportunity cost.

- Missed Investment Opportunities: Historically, the stock market often yields higher annual returns than property appreciation. If you invest your cash in a diverse portfolio and take out a mortgage instead, you might mathematically end up wealthier in the long run, even after paying mortgage interest.

- No Tax Perks from Government Schemes: If you use all your cash, you might miss out on specific government bonuses, such as the additions provided by a Lifetime ISA, which are designed to help people build deposits rather than buy outright.

- Risk of Overpaying: Lenders act as a safety net because they will not let you borrow more than a house is strictly worth. Without a bank looking over your shoulder, you run the risk of letting your emotions guide you and overpaying for a property.

- Higher Stamp Duty for Luxury Homes: If you are buying a second home or an investment property with cash, you will face significant Stamp Duty surcharges.

Step-by-Step Process: How to Buy a House with Cash UK in 2026

If you have weighed the pros and cons and decided that a cash purchase is the right move for you, it is time to look at the roadmap. The cash house purchase UK process is beautifully streamlined compared to getting a mortgage, but you still need to follow specific legal steps. Let us break down exactly how you buy a house with cash.

Find Your Dream Home and Make an Offer

Your journey begins exactly like anyone else’s. You will scour property portals like Rightmove and Zoopla, attend viewings, and explore neighbourhoods. Once you find the perfect place, you make an offer to the estate agent.

This is where you play your trump card. Tell the estate agent you are a cash buyer and have no property chain. This makes your offer incredibly attractive. However, the agent will not just take your word for it. You must provide proof of funds. This usually means handing over a recent bank statement or a letter from your accountant showing that you have the liquid cash ready to go.

Instruct Your Property Professionals

Once the seller accepts your offer, you need to bring in the professionals. Since you are paying cash, you can completely skip the mortgage broker. However, you absolutely must hire a solicitor or a conveyancer.

Conveyancing is the legal process of transferring property ownership from one person to another. Your solicitor will handle all the complex legal paperwork, draft the contracts, and ensure the seller actually has the legal right to sell you the home. Expect to pay between £1,200 and £2,500 for a good conveyancer. Do not skimp on this step; a brilliant solicitor is worth their weight in gold for a fast, smooth transaction.

Conduct Essential Surveys and Local Searches

A common myth is that cash buyers do not need surveys. While it is true that no bank will force you to get one, buying a house without a survey is a terrible idea. You are spending hundreds of thousands of pounds; you need to know what is hiding behind the walls.

Hire an independent surveyor to conduct a Homebuyer’s Report (RICS Level 2 or 3). They will check for structural issues, dampness, subsidence, and roof problems. Simultaneously, your solicitor will conduct local authority searches. These searches reveal vital information about the local area, such as planned roadworks, flood risks, and whether the property sits on contaminated land.

The Exciting Part – Exchanging Contracts

Once your solicitor finishes the searches and you are happy with the survey results, you reach the point of no return: exchanging contracts.

Your solicitor will sit down with the seller’s solicitor and swap the signed legal documents. At this exact moment, the transaction becomes legally binding. You will transfer a 10% deposit to your solicitor, who holds it safely. If you back out of the sale after this point, you lose your deposit and can face legal action. If the seller backs out, you can sue them. This step provides massive security for everyone involved.

Completion Day and Getting Your Keys

Completion day is the day you officially become a homeowner! You and the seller will agree on this date when you exchange contracts.

On completion day, your solicitor will take the remaining 90% of your funds and transfer them to the seller’s solicitor using a secure CHAPS bank transfer (which usually costs around £30). Once the seller’s solicitor confirms they have received the money, the estate agent will call you with the best news ever: your keys are ready to collect. You can now move into your new home.

Registering with the Land Registry

Even though you have the keys, there is one final piece of admin left. Your solicitor will register you as the new legal owner of the property with HM Land Registry.

This process involves paying a fee (usually between £100 and £500, depending on the property’s value). Because the Land Registry is often backlogged, it might take anywhere from four to eight weeks for the paperwork to officially clear. However, do not worry—this happens in the background, and you can comfortably enjoy your new home while you wait.

Costs Involved: Budgeting for a Cash House Purchase in the UK

One of the great joys of buying with cash is avoiding lender fees. However, the purchase price of the house is not the only money you will spend. You must set aside a healthy budget for taxes, legal fees, and moving costs.

To help you plan, here is a detailed breakdown of the extra costs you can expect when buying a house with cash in the UK in 2026.

Cost Type Estimated Amount (2026)Notes

Stamp Duty Land Tax (SDLT) 0% under £250K; 5% £250-925 K. Always use the official government calculator to check your exact rate.

Legal Fees (Conveyancing) £1,200 – £2,500. Ask for fixed-fee quotes so you do not get surprised by hourly billing.

Property Surveys £400 – £1,500, depending on the size of the house and if you choose a RICS Level 2 or 3 survey.

HM Land Registry Fee £100 – £500 Scales based on the total value of the property you are buying.

Moving and Setup Costs £1,000 – £5,000. Includes removal vans, initial home insurance, and basic immediate repairs.

Total Extra Cash Needed £3,000 – £10,000+ This is the average extra cash needed for a standard £400,000 home (excluding SDLT variables).

Navigating Taxes and Hidden Fees

Let us talk a bit more about the biggest expense on that list: Stamp Duty Land Tax (SDLT). Whether you buy with a mortgage or with cash, you must pay Stamp Duty. If you are a first-time buyer purchasing a home under a certain threshold, you might qualify for fantastic tax relief, meaning you pay absolutely nothing. However, if this is a second home or a buy-to-let investment, you will face a 3% surcharge on top of the standard rates. Always consult a tax professional or use the government’s online calculator before you commit your funds.

You should also budget for hidden costs. When your surveyor hands you their report, they might flag that the boiler is on its last legs or the roof needs minor patch repairs. Because you are buying with cash, you will need extra liquid funds set aside to handle these immediate post-purchase repairs.

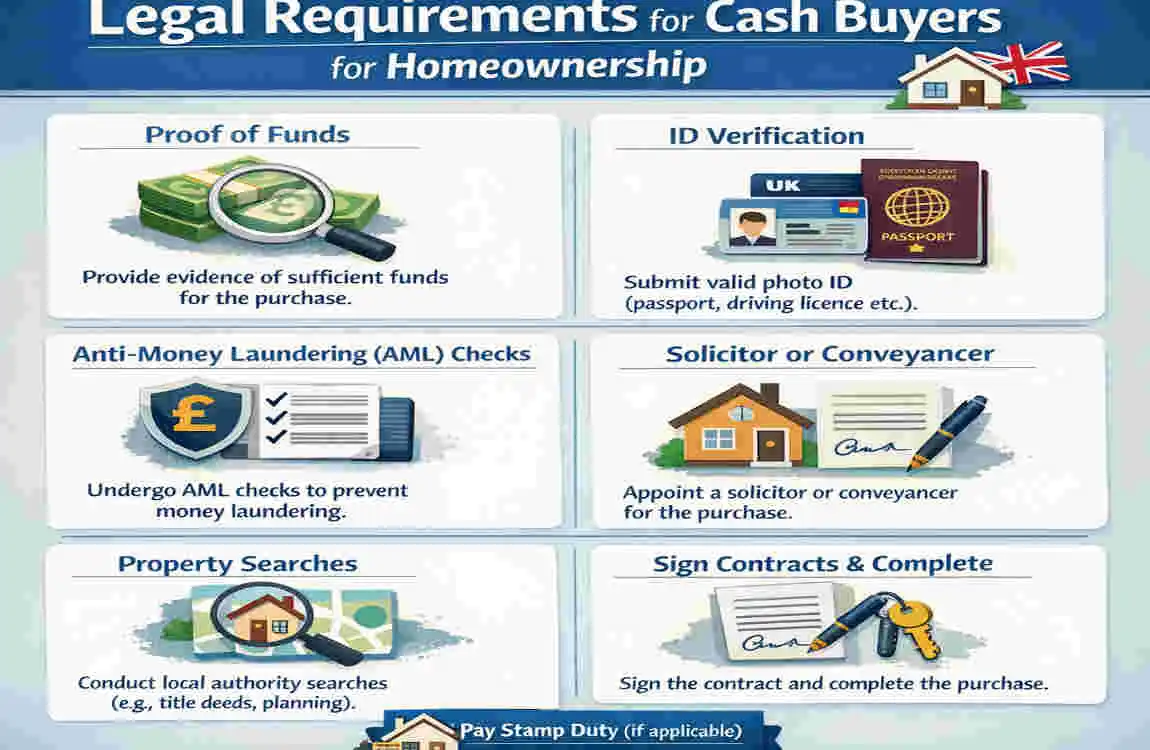

Legal Requirements for Cash Buyers in the UK

The property market is heavily regulated to prevent fraud and illegal activity. Even though you are bypassing the bank’s strict checks, you cannot bypass the UK government’s legal requirements. Here is what the law demands of you as a cash buyer.

Proving Where Your Money Comes From

The most rigorous check you will face is the Anti-Money Laundering (AML) check. The UK government requires all solicitors and estate agents to verify exactly where your cash originated. They do this to ensure criminals are not using the property market to launder dirty money.

You cannot simply show a bank statement with a massive lump sum on it. Your solicitor will ask you to provide a paper trail. If you saved the money from your salary, they will want to see months of payslips and bank statements. If you sold a business, they will want the sale documents. If you inherited the money, you will need a letter from the executors of the will. Be prepared to be fully transparent about your finances; it is a standard legal requirement, and your solicitor is just doing their job.

Standard Contracts and Forms

During the conveyancing process, you will encounter several standard legal forms. The most common are the TA6 (Property Information Form) and the TA10 (Fittings and Contents Form).

The seller fills these out to tell you exactly what is included in the sale. Will they leave the washing machine? Are the garden fences their responsibility to fix? Have they had any disputes with the neighbours? Your solicitor will review these forms with you to ensure you are completely happy with the terms before you exchange contracts.

Special Rules for Overseas Buyers

If you are an expat or a foreign national buying UK property with cash, you face an extra layer of legal scrutiny. Solicitors must conduct enhanced due diligence to verify international funds. Furthermore, you will likely face an additional 2% Stamp Duty surcharge, which the government applies to non-UK residents buying residential property.

Cash vs. Mortgage: Which is Best for UK Homeownership?

Now that we have covered the “how,” you might still be debating the “why.” If you have the cash available, should you use it, or should you take out a mortgage and keep your cash in the bank? Let us compare the two paths so you can make the smartest choice for your lifestyle.

Evaluating Speed, Costs, and Risks

If your primary goal is speed and simplicity, cash wins every single time. You cut out the middleman, you eliminate the risk of a lender down-valuing the property, and you skip the massive interest payments.

However, if your primary goal is growing your overall wealth, a mortgage might be the smarter play. Mortgages allow you to use leverage. You can put down a 20% deposit and borrow the rest. This leaves 80% of your cash free to invest in the stock market, start a business, or even buy a second investment property.

With the Bank of England base rates fluctuating around 4.5% in 2026, you have to do the math. If your investment portfolio yields a 7% return, but your mortgage interest is 5%, you are technically making a profit by taking out a mortgage and investing your cash.

Which Option Fits Your Lifestyle?

Ultimately, the choice comes down to your personal comfort level.

If you are a retired couple looking to downsize and enjoy a stress-free life without monthly debt hanging over your head, buying with cash is a brilliant, freeing decision. The peace of mind that comes with knowing nobody can take your home away is invaluable.

If you are a young professional or a property investor trying to build an empire, using a mortgage to leverage your cash across multiple properties will help you grow your portfolio much faster.

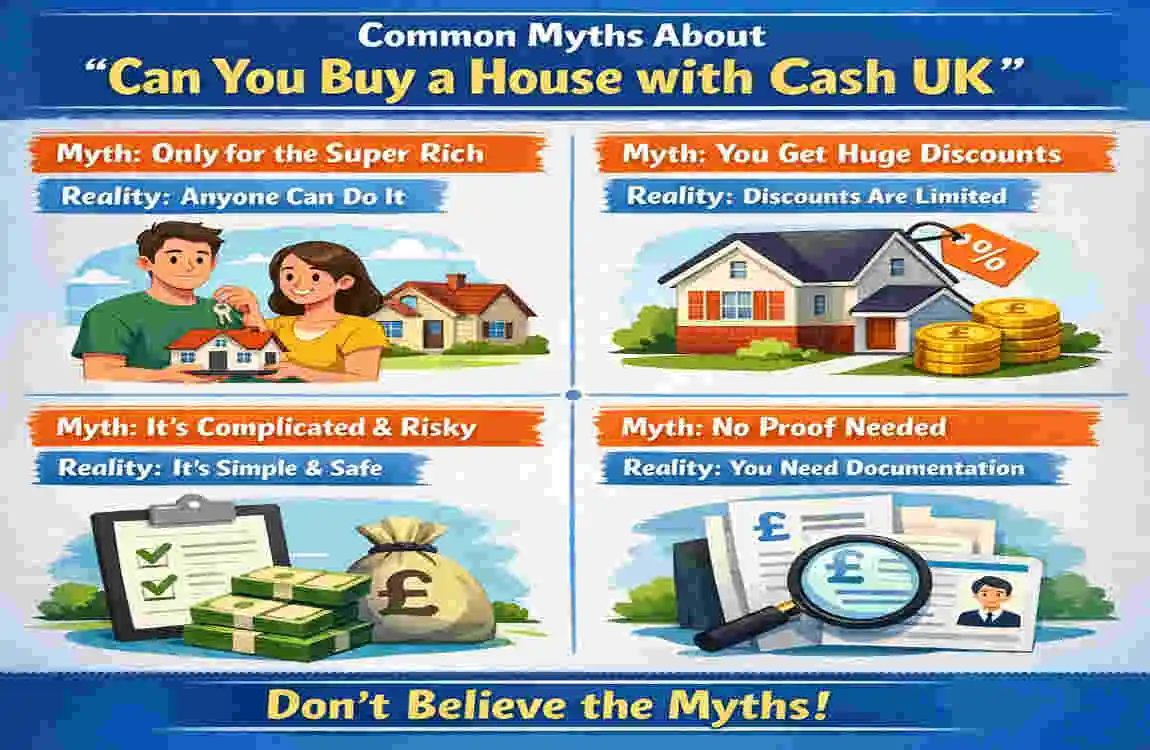

Common Myths About “Can You Buy a House with Cash UK”

Because cash buying is a bit of a mystery to those who have never done it, several misconceptions float around the property market. Let us bust the biggest myths right now.

Busting the Biggest Cash Buyer Misconceptions

You do not need to bother with property surveys. We mentioned this earlier, but it bears repeating. Skipping a survey just because a bank isn’t forcing you to get one is a fast track to financial disaster. A £500 survey could save you from buying a house with £30,000 worth of hidden roof damage. Always get a professional to inspect the property.

Cash buys mean instant ownership. Many people think that if they have cash, they can buy a house in a weekend. False! You still have to go through the legal conveyancing process. Local searches take time, drafting contracts takes time, and proving the source of your funds takes time. While an 8-week timeline is much faster than a mortgage purchase, it is certainly not instantaneous.

Buying with cash is always cheaper overall. While you save money on mortgage interest, you lose money on opportunity cost. If you sink £400,000 into a house, that money is no longer earning you interest in a high-yield savings account or stock portfolio. You have to factor in what that money could have earned you before declaring cash the absolute cheapest route.

Tips for Fast-Track Success as a Cash Buyer UK

If you are ready to move forward, you want to ensure your cash purchase goes as smoothly as possible. Here are a few insider tips to help you maximise your advantage and secure your new home without a hitch.

Making Your Cash Offer Irresistible

- Pre-Approve Your Solicitor: Do not wait until your offer is accepted to start looking for a conveyancer. Find a great solicitor early, get their contact details ready, and instruct them the moment the estate agent calls you with good news. This shows the seller you mean business.

- Line Up Your Proof of Funds: Have your bank statements and your accountant’s letters ready in a digital folder. When you make your offer, attach your proof of funds immediately. This eliminates any doubt in the estate agent’s mind.

- Offer for Speed, Not Just Price: You have incredible negotiating power. If a seller is desperate to move quickly because they are relocating for work or going through a divorce, they will often accept a lower cash offer over a higher mortgage offer. Remind them that you can complete the sale in a matter of weeks, not months.

- Use Cash-Friendly Agents: Look for properties listed with estate agents that cater heavily to fast sales, like Purplebricks or specialised auction houses. These agents know exactly how to handle cash buyers and will help push the legal paperwork through quickly.

- Keep Liquid Cash for Emergencies: Do not empty your bank account completely. Always ensure you have a comfortable emergency fund left over after paying for the house, the taxes, and the legal fees. Homeownership always comes with unexpected maintenance costs!

FAQs: Can You Buy a House with Cash in the UK?

To wrap up all this information, let us answer some of the most frequently asked questions about the cash house purchase process in the UK.

Can you buy a house with cash in the UK without using a solicitor? No, you really cannot. While you might theoretically be able to navigate the legal jargon yourself, it is incredibly risky and highly discouraged. A certified solicitor or conveyancer is mandatory to legally transfer the property title, handle the Land Registry updates, and perform anti-money laundering checks.

How long does a cash house purchase take? On average, a cash purchase in the UK takes between 8 and 12 weeks. If there is no property chain and local searches come back quickly, it can occasionally be done in 4 to 6 weeks.

Do cash buyers pay less Stamp Duty? No. Stamp Duty Land Tax is based on the purchase price of the property and your status as a buyer (e.g., first-time buyer, second-home owner). The government does not care whether you use cash or a mortgage; the tax rates remain exactly the same.

What if my funds are coming from selling my current home? If you have to sell your home to get the money, you are technically involved in a property chain. While you won’t need a mortgage for the new house, estate agents will view you as a “cash buyer subject to sale.” True cash buyers have the funds sitting completely liquid in their bank accounts right now.