If you are asking yourself, how long does it take to buy a house in the fast-paced market of 2026, you are certainly not alone. The journey from casually browsing property listings on your phone to finally unlocking the front door of your dream home is incredibly exciting. Still, it can also feel like an unpredictable rollercoaster. You might have heard stories from friends who closed on a house in just a few weeks, while others spent the better part of a year trapped in endless paperwork and bidding wars.

So, what is the real answer? In today’s competitive real estate landscape, rising buyer demand and fluctuating interest rates mean timelines can vary widely. On average, the entire home-buying process takes 2 to 6 months. This timeframe includes everything from your very first financial check-up to the glorious day you receive your keys.

We know that waiting is the hardest part. You want to plan your move, buy your furniture, and start your new life. That is exactly why understanding the complete timeline is your best weapon. When you know what is coming next, you can prepare your documents, anticipate common roadblocks, and actually speed up the entire process.

Standard Home Buying Timeline

To truly understand how long it takes to buy a luxury house, we need to split the process into two main phases: the pre-offer search and the post-offer closing.

Most buyers spend roughly 1 to 3 months just hunting for the right property. This is the fun part! You get to tour neighbourhoods, imagine your life in different spaces, and figure out what features you cannot live without.

Once you find “the one” and the seller accepts your offer, the clock resets. The secondary phase—going from offer acceptance to closing day—typically takes a rigid 30 to 60 days. This is when the heavy lifting happens behind the scenes with lenders, inspectors, and lawyers.

To give you a clear, visual understanding of the journey ahead, take a look at this standard Gantt-style breakdown of the average timeline:

Stage Expected Duration Key Tasks Involved

Pre-Approval 1 to 3 weeks: Credit checks, gathering lender documents, and budget planning

House Search 4 to 12 weeks: Online browsing, attending viewings, meeting with your agent

Offer to Closing 30 to 60 days Negotiations, home inspection, property appraisal, and loan underwriting.

Keep in mind that these are average estimates. If you are extremely prepared or paying entirely in cash, you can absolutely crush this timeline and move in much faster. Let’s break down each specific step to see exactly where your time goes.

Financial Preparation and Pre-Approval

Before you even look at a single house, you need to get your finances in perfect order. This initial stage usually takes between 2 and 4 weeks, but it is the most critical step to shorten the overall time to buy a house. If you skip this, you will face significant delays later.

Gathering Your Financial Documents

Lenders want proof that you are a reliable borrower. To get a mortgage pre-approval, you need to show them exactly how much money you make and how much you have saved. You should gather your recent pay stubs, W-2 forms (or local tax equivalents), and at least two months of bank statements. If you are self-employed, prepare to hand over two years of detailed tax returns. By collecting these documents now, you prevent your lender from pausing your application later to request missing paperwork.

The Impact of Your Credit Score

Your credit score acts as your financial report card. Most standard lenders look for a score of 620 or higher. If your score is lower, it might take you a few extra months to pay down existing debts and boost your score. A higher credit score not only speeds up the approval process but also unlocks lower interest rates, saving you thousands of dollars over the life of your loan.

Local Market Nuances: Lahore and the State Bank

If you are looking to buy in vibrant, expanding markets like Lahore, , local banking regulations play a massive role in your timeline. Mortgage options have evolved, but processing times heavily depend on the State Bank (SBP) current policy rates and lending guidelines. Local banks may require extra time to verify income, especially for overseas buying property back home. Preparing your income certificates, Roshan Digital Account details (if applicable), and tax records early will keep your Lahore property dreams right on schedule.

Finding the Right House

Once you have your pre-approval letter, the hunt officially begins. On average, this phase takes 1 to 2 months, but highly motivated buyers can easily cut this down to 4 weeks using modern tools.

Leveraging Online Real Estate Tools

Gone are the days of driving around neighbourhoods looking for “For Sale” signs. Today, your search starts on your smartphone. Using robust online platforms lets you filter homes by price, location, number of bedrooms, and even specific amenities. For buyers, utilising portals like Zameen.com is an absolute game-changer. You can track pricing trends in popular areas like DHA or Bahria Town, helping you understand the market before you ever set foot inside a house.

Selecting the Right Real Estate Agent

You need an expert in your corner. A seasoned real estate agent does not just open doors for you; they act as your local market guide, negotiator, and timeline enforcer. Take a few days to interview potential agents. Ask them about their experience in your desired neighbourhoods. A proactive agent will curate a targeted list of homes for you, saving you from wasting weekends looking at properties that do not fit your criteria.

Embracing Virtual Tours

In 2026, technology is your best friend for saving time. High-definition 3D virtual tours allow you to “walk through” a property from your couch. You can instantly eliminate houses with weird floor plans or tiny kitchens without spending an hour commuting across town. By the time you actually visit a house in person, you already know it is a strong contender.

Making an Offer and Negotiations

You found the perfect house! Now, you must convince the seller to give it to you. This step happens fast. In a hot market, the time from drafting your offer to acceptance can take anywhere from 1 to 7 days.

Competitive Bidding Strategies

When you find a great house, chances are someone else likes it, too. Your real estate agent will help you review recently sold comparable homes in the area to determine a fair and competitive offer price. If the market is fiercely competitive, you should offer slightly above the asking price or write a personalised letter to the seller explaining why you love their home.

Understanding Contingencies

Contingencies are your safety nets. They are conditions set out in the contract that must be met for the sale to go through. Common contingencies include a satisfactory home inspection and your ability to secure final financing. While contingencies protect you, having too many can make your offer look weak to a seller. If you want to speed up acceptance, work with your agent to include only the necessary contingencies.

Home Inspection and Appraisal

Once the seller accepts your offer, your contract is officially active. The clock starts ticking immediately on your inspection and appraisal phase, which usually takes 10 to 14 days. Delays here can easily add weeks to your home-buying timeline, so you must act quickly.

Identifying Deal-Killing Red Flags

You should always hire a licensed, independent home inspector. Their job is to crawl into the attic, check the plumbing, inspect the roof, and test the electrical systems. They will provide a detailed report of everything wrong with the house. While chipped paint is no big deal, serious red flags like a cracked foundation, massive water damage, or outdated wiring can bring the whole deal to a grinding halt.

Renegotiation Tactics

If the inspector finds major issues, you have a choice. You can walk away, accept the house as-is, or renegotiate. Renegotiating takes time. You might ask the seller to fix the broken roof before closing, or you might ask them to lower the purchase price so you can fix it yourself. Back-and-forth negotiations can add several days to your timeline, but it is always worth the wait to avoid buying a money pit.

The Appraisal Process

While you care about the house’s physical condition, your mortgage lender cares about its financial value. The bank will hire an appraiser to ensure the house is actually worth the amount of money you are borrowing. If you offer $300,000 for a house, but the appraiser says it is only worth $280,000, you have an “appraisal gap.” Resolving this gap—either by the seller dropping the price, you paying the difference in cash, or challenging the appraisal—is a common hurdle that can extend your timeline.

Underwriting and Final Approval

Welcome to the longest and quietest phase of the home-buying process. Mortgage underwriting usually takes 21 to 30 days. Because all the action happens behind closed doors at the bank, many buyers feel anxious during this time.

What Actually Happens During Underwriting?

Think of the underwriter as a financial detective. Even though you were pre-approved weeks ago, the underwriter must now verify every single detail of your financial life with absolute certainty. They will double-check your employment, scrutinise your bank deposits, verify the property appraisal, and ensure you meet all loan guidelines. They are making sure nothing has changed since your initial application.

Common Delays During This Phase

This is the stage where the answer to “how long does it take to buy a house” can jump from 30 days to 60 days if you make a mistake. The biggest cause of delay? Buyers are making sudden financial changes. If you suddenly quit your job, take out a massive auto loan to buy a new truck, or open three new credit cards to buy furniture, the underwriter will flag your file. Any new debt changes your debt-to-income ratio. This forces the bank to recalculate your entire loan, causing massive delays and potentially ruining your mortgage approval altogether.

How to Expedite Final Approval

To get through underwriting quickly, follow the golden rule: keep your finances completely frozen. Do not move large amounts of money between accounts without a paper trail. Do not buy large items on credit. Furthermore, if the underwriter emails you asking for an updated pay stub or a letter explaining a past address, respond immediately. Your speedy replies keep your file at the top of their desk.

Closing Day

You made it! The bank has issued a “Clear to Close.” The actual closing day takes only 1 day (usually just a few hours), but the preparation takes about a week.

The Final Walkthrough

About 24 to 48 hours before you sit down to sign the papers, you will do a final walkthrough of the property. This is your chance to verify that the seller has fully moved out, they left behind the appliances they promised, and they actually completed the repairs agreed upon after the inspection. If you find a large hole in the wall that wasn’t there before, your agent will need to pause the closing until the issue is resolved.

Signing the Documents and Funding

On closing day, you will sit in a room (or jump on a secure video call) with your real estate agent, maybe a lawyer, and a title agent. Get ready to sign your name dozens of times. You will sign the mortgage agreement, the property title transfer, and various legal disclosures. Once the ink is dry, your lender wires the funds to the seller. As soon as the transaction is officially recorded with the local government, the keys are handed over. The house is finally yours!

Factors Affecting the Timeline

By now, you understand the standard steps. But how long does it take to buy a house when life throws curveballs? Several major variables can either drastically shrink or significantly expand your timeframe.

Current Market Conditions

Real estate markets operate based on supply and demand. In a seller’s market—where there are more buyers than available homes—houses sell incredibly fast. You might find yourself pressured to make quick decisions, shortening the search phase. However, you might also face multiple rejections from bidding wars, which can drag your search out for months. Conversely, in a buyer’s market, you have the luxury of time to browse, but sellers might drag out negotiations.

Financing Type: Cash vs Mortgage

Cash is king when it comes to speed. If you have enough money in the bank to buy a house outright without a mortgage, you bypass the entire pre-approval, appraisal, and underwriting process. A cash transaction can easily be closed in just 7 to 14 days. For everyone else relying on bank financing, you are bound by the lender’s 30- to 45-day processing schedule.

Location Matters: Urban Centres vs Suburbs

Where you choose to live impacts how long you wait. If we look at a bustling metropolitan area like Lahore, buying a modern apartment in the city centre, such as Gulberg, might involve swift digital transactions and fast-moving developers. On the other hand, buying a plot or home in the expanding suburbs or newer phases of DHA might require more extensive background checks, title verifications, and physical document processing by local land authorities.

Buyer Readiness and Experience

Let’s be honest: first-time home buyers usually take about 30 days longer than experienced buyers. If this is your first time, you naturally need more time to understand the terminology, compare loan types, and feel comfortable signing massive financial contracts. Experienced buyers already know what they want and have their documents ready to fire off at a moment’s notice.

Market Trends Shaping Your Timeline

The real estate industry is evolving rapidly, and 2026 brings some fascinating trends that directly affect the time it takes to buy a house.

The Rise of Digital Closings

One of the most exciting shifts is the widespread adoption of digital closings. In the past, mailing physical documents back and forth to lawyers and banks added weeks to the timeline. Now, secure e-signatures and digital notarizations can shave up to 10 days off your closing process. Lenders are using automated underwriting systems powered by AI that can verify your bank statements in seconds rather than days.

Fluctuating Interest Rates

As global interest rates continue to adjust in 2026, buyers are rushing to lock in favourable rates before they rise. This urgency is pushing the average closing time closer to a brisk 40-day average for well-prepared buyers. Lenders are motivated to process loans quickly, and buyers are motivated to provide documents faster to secure their quoted rates.

Tips to Speed Up the Process

Nobody wants to live in a state of limbo. If you want to reduce your total home-buying time by up to 30%, you need to be proactive. Here is an actionable list of strategies to fast-track your journey:

- Get Pre-Approved Early: Do this before you even look at houses. A pre-approval letter proves to sellers that you are a serious, funded buyer.

- Keep Your Must-Have List Short: If you refuse to buy a house unless it has a pool, a three-car garage, and a south-facing garden, you will be searching for a very long time. Be flexible.

- Limit Your Contingencies: If you are in a competitive market, consider waiving non-essential contingencies. Just be sure to consult your agent so you do not expose yourself to massive financial risk.

- Use Digital Tech: Download scanner apps on your phone so you can instantly upload W-2s, pay stubs, and IDs to your lender’s secure portal the moment they request them.

- Choose Experienced Professionals: An experienced real estate agent and a highly-rated local mortgage broker have established relationships. They know exactly who to call to expedite paperwork through the system.

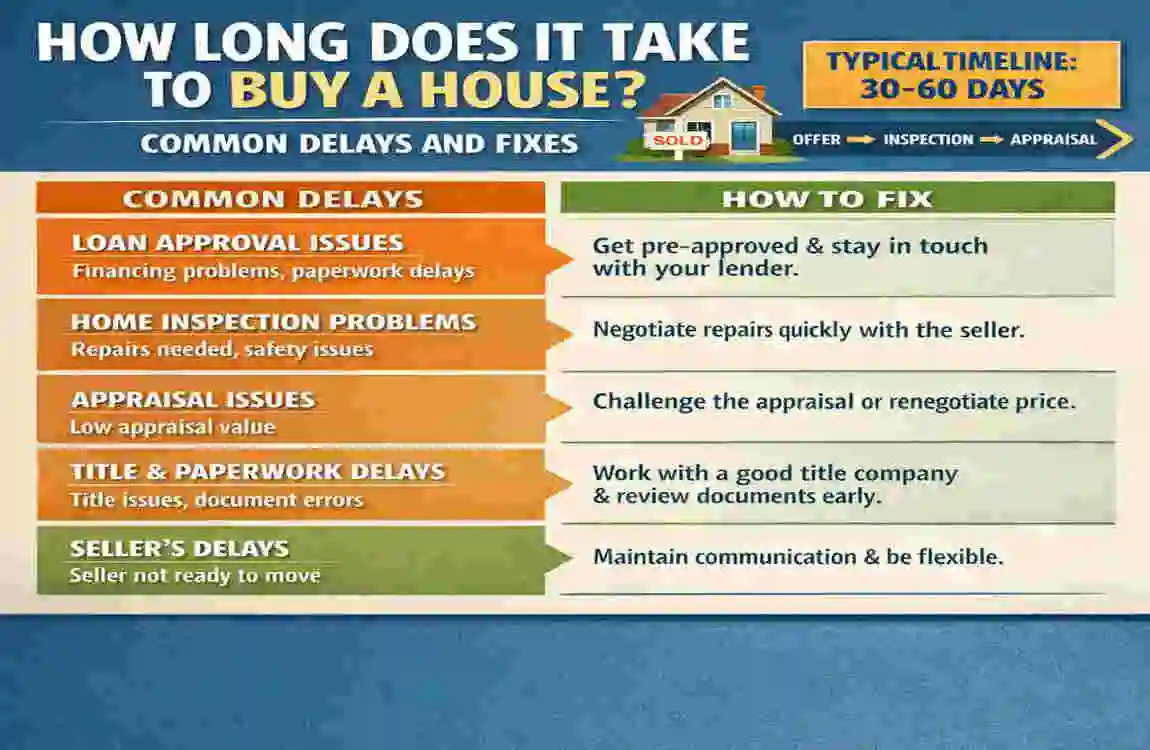

Common Delays and How to Fix Them

Even with perfect planning, roadblocks happen. Knowing how to handle these common pitfalls will prevent a small delay from ruining your deal.

The Dreaded Title Issues

Before you buy a house, a title company researches the property to ensure the seller actually owns it free and clear. Sometimes, they discover unresolved liens, unpaid property taxes, or legal claims from a past relative. This can easily add 2 to 3 weeks to your timeline.

- The Fix: You cannot prevent a seller’s title issue, but you can insist that the title search is ordered the very same day your offer is accepted. The sooner they start searching, the sooner the seller’s lawyers can resolve any issues.

The Appraisal Falls Short

As mentioned earlier, if the bank thinks the house is worth less than your offer, they will not lend you the full amount.

- The Fix: Ask your agent to provide “comps” (comparable recent sales) to the appraiser to justify your offer price. If that fails, be prepared to negotiate a middle-ground price with the seller immediately to keep the timeline moving.

Final Walkthrough Surprises

You do your final walkthrough and realise the seller ripped out the custom chandeliers they agreed to leave behind.

- The Fix: Do not delay the entire closing over a small aesthetic issue. Instead, ask your lawyer to withhold a specific amount of the seller’s proceeds in an escrow account until the items are returned or paid for. You still get your keys on time, and the financial dispute is handled safely.

Cost Breakdown by Timeline

You might be thinking, “Why does it matter if it takes 30 days or 90 days? I’ll get the house eventually.” The truth is, time is money in real estate. An extended house-buying process can actually drain your wallet through higher rent payments, storage unit fees, and shifting interest rates.

Let’s look at how the length of your timeline impacts your hidden costs:

Timeline Scenario Average Hidden Costs Primary Cost Drivers Savings Tip

Fast (30 Days) Low ($2K – $5K) Basic closing fees, immediate moving truck rental. Opt for a Cash deal or use local digital lenders for instant processing.

Average (60 Days) Medium ($5K – $8K) One extra month of rent, rate-lock extension fees. Organise documents early to avoid lender delays.

Slow (90+ Days) High ($10K+) Multiple months of rent, storage unit fees, and higher interest rates if your initial rate lock expires. Get pre-approved fast and respond to underwriter emails within hours.

By working efficiently and keeping your timeline tight, you keep more money in your bank account to spend on painting, decorating, and enjoying your new home.

Frequently Asked Questions (FAQs)

As you navigate this journey, you likely have some specific concerns. Here are the most common questions buyers ask when figuring out how long it takes to buy a house.

How long does it take to buy a house with bad credit?

If your credit score is below 620, the process takes significantly longer. You should expect to add 3 to 6 months to your timeline. This extra time is necessary to pay off high credit card balances, dispute errors on your credit report, and build a history of on-time payments so a lender feels comfortable giving you a mortgage.

What is the difference between cash and mortgage timelines?

A cash buyer avoids the entire bank underwriting and appraisal process. Because they do not need a lender’s approval, a cash purchase can comfortably close in 7 to 14 days, mostly waiting on the legal title search. A mortgage buyer must undergo financial verification, which forces the timeline to a strict 30 to 60-day minimum.

Are there any specifics about first-time buyers I should know?

Yes! First-time buyers often qualify for special government assistance programs or lower down payment options. However, these specialised loan programs usually require extra layers of bureaucratic approval. First-time buyers should realistically expect to add about 15 to 30 days to their house hunting and closing phases compared to veteran buyers.

Can a seller back out and delay the process?

It is very rare and legally difficult for a seller to back out once a contract is signed, unless you (the buyer) fail to meet your deadlines. If the seller tries to delay because they haven’t found a new home to move into, you can negotiate a “rent-back” agreement: you buy the house on time but rent it back to them for a month, so you do not lose your interest rate lock.

How quickly can I move in after closing?

In most standard contracts, you receive the keys the same day you sign the closing paperwork and the loan funds are transferred. You can literally drive from the lawyer’s office to your new house and start moving boxes inside that afternoon!