You have probably found yourself scrolling through endless listing photos of older houses, sighing at the outdated kitchens or weird layouts, and asking yourself the big question: “Is now a good time to build a home in 2026?”

It is the dream, isn’t it? Designing a space that is perfectly tailored to your life, where no one else has ever lived. But with the economy tossing us curveballs every few months, making that leap feels like a massive decision.

Here is a quick reality check to get us started: According to recent data from the National Association of Realtors (NAR), U.S. home prices have continued to tick up by about 5% year-over-year. While that sounds pricey, it also means investing in real estate is still a solid bet for building wealth.

Current Housing Market Snapshot: Why Timing Matters in 2026

Before we start picking out tile samples or looking at floor plans, we have to look at the bigger picture. The housing market in 2026 is a different beast than it was just a few years ago.

If you remember the chaos of 2021 and 2022, you might be gun-shy. Back then, materials were impossible to find, and prices were skyrocketing by the day.

The good news? Things have calmed down. The supply chains that were once knotted up are flowing again. However, we are facing new challenges that affect whether it is a good time to build a home.

The Mortgage Rate Landscape

Interest rates are the elephant in the room. As of early 2026, mortgage rates have settled into the 6.2% to 6.5% range. While this isn’t the rock-bottom 3% we saw years ago, it is an improvement over the peaks of 2024.

This stability allows you to budget more accurately. You aren’t guessing if your rate will jump two points overnight.

Inventory Is Still Tight

Here is why building is so attractive right now: there aren’t enough existing houses for sale. This is a global issue, whether you are looking in the suburbs of Austin, Texas, or checking out growing housing societies in places like Lahore, Pakistan.

When inventory is low, bidding wars happen. Building a custom home lets you avoid that competition entirely.

Inflation and Material Costs

Are we still paying $10 for a 2×4? Thankfully, no. Lumber and concrete prices have stabilized. While labor is still pricey (we will get to that later), the actual “stuff” your house is made of is more affordable than it was during the pandemic peak.

Here is a look at how the market has shifted over the last three years to help you visualize the trend.

2024-2026 Market Comparison

Year Avg. Home Price Mortgage Rate (Avg)New Builds Started

2024 $400,000 6.8% 1.2 Million

2025 $420,000 6.5% 1.4 Million

2026 $440,000 (Proj.) 6.2% 1.5 Million (Proj.)

Pros of Building a Home Right Now

There is a lot of optimism in the construction industry this year. If you ask a developer, ” Is now a good time to build a home?” they will give you a resounding “Yes.” But why?

Here are four compelling reasons why 2026 might be your year to build.

Lower Material Costs Post-Pandemic

One of the biggest wins for builders right now is the cost of materials. During the pandemic, supply chain issues caused prices for lumber, steel, and copper to hit historic highs.

In 2026, those supply chains are healed.

Lumber prices have dropped significantly from their 2022 peaks. This means your budget stretches further. You can afford those hardwood floors or the quartz countertops that would have been out of reach a few years ago.

Additionally, because materials are readily available, you are less likely to face agonizing months-long delays when your house frame sits there in the rain, waiting for windows to arrive.

Customization in a Seller’s Market

When you buy an existing home in a seller’s market, you often have to settle. You might get the right neighborhood, but hate the kitchen. Or you get the right number of bedrooms, but the roof needs to be replaced in two years.

Building gives you total control.

You can prioritize what matters to you now.

- Need a dedicated home office for remote work? Build it.

- Want a multi-generational suite for aging parents? Design it.

- Want a solar-ready roof to save on bills? Plan for it.

In 2026, energy efficiency will be a major focus. New building codes mean your new home will be far better insulated and cheaper to cool and heat than a house built even ten years ago. This saves you money every single month.

Potential Rate Drops Ahead

This might sound counterintuitive, but hear me out. Rates are currently hovering around 6.5%. However, the Federal Reserve has signaled that if inflation remains tamed, rate cuts could be on the horizon later in the year or into 2027.

There is a saying in real estate: “Marry the house, date the rate.”

If you build now, you lock in the construction price. If rates drop by the time your home is finished (which usually takes 8 to 12 months), you can refinance or lock in a lower rate for your final mortgage. Plus, there are various tax incentives, especially for “green” building practices (like the Inflation Reduction Act credits), that can put money back in your pocket.

Long-Term Value in Growing Areas

Real estate usually appreciates over time. New construction often appreciates faster in the early years because everything is brand-new and under warranty.

If you are looking at up-and-coming areas—think suburban booms just outside major tech hubs or growing metropolitan areas—getting in early can be a goldmine.

According to Zillow data, new homes in developing subdivisions can appreciate roughly 7% faster than older homes in stagnant neighborhoods. You are building equity from the day you break ground.

Cons of Building a Home in 2026

We need to be honest with each other. It isn’t all sunshine and fresh paint. There are genuine risks involved. To truly answer “is now a good time to build a home,” we have to look at the darker side of the coin.

Here are the hurdles you will need to jump over.

High Upfront Costs and Financing Hurdles

Financing a new build is more complicated than getting a standard mortgage. You typically need a construction loan, which often comes with higher interest rates (sometimes 7-8%) during the building phase compared to a standard 30-year fixed mortgage.

Furthermore, you usually have to pay “interest-only” payments on the money drawn out during construction, while also paying for your current living situation (rent or mortgage). That double payment can strain even a healthy budget.

Total build costs in 2026 are estimated to range between $150 and $400 per square foot, depending on your finishes and location. That is a steep entry price.

Labor Shortages and Timeline Risks

While materials are cheaper, labor is the new bottleneck. The construction industry is facing a “Silver Tsunami”—older skilled tradespeople (electricians, plumbers, framers) are retiring, and there aren’t enough young workers replacing them.

The Associated General Contractors of America (AGC) has noted a shortfall of hundreds of thousands of workers.

What does this mean for you?

- Delays: If the plumber is booked solid for three weeks, your project stalls.

- Costs: High worker demand means they charge more.

- Weather: If labor delays push your build into the rainy or snowy season, you face weather delays that can add 10-20% to your timeline.

Market Uncertainty: Recession Fears

Economists love arguing over whether a recession is coming. While 2026 looks relatively stable, there is always a lingering fear of an economic downturn.

If the economy takes a nosedive just as you finish building, the value of your new home could dip temporarily. While real estate is a long-term game, it can be scary to see your appraisal come in lower than your construction cost if the market flips.

There is also the “opportunity cost.” If you buy an existing home today, you can move in in 30 days. Building takes a year. That is a year of your life spent managing a project.

Hidden Fees Eating Budgets

The price on the contract is rarely the price you pay. If you have never built before, the “hidden” costs can be a shock.

We aren’t just talking about upgrading to nicer countertops. We are talking about unsexy things like soil testing, permits, bringing utilities to the site, and unexpected excavation issues.

You need a contingency fund. Here is a rough breakdown of where your money actually goes in 2026:

Home Building Cost Breakdown

Category% of Total Budget2026 Avg Cost (Example)

Materials 50% $150,000

Labor 30% $90,000

Land/Permits/Fees 20% $60,000

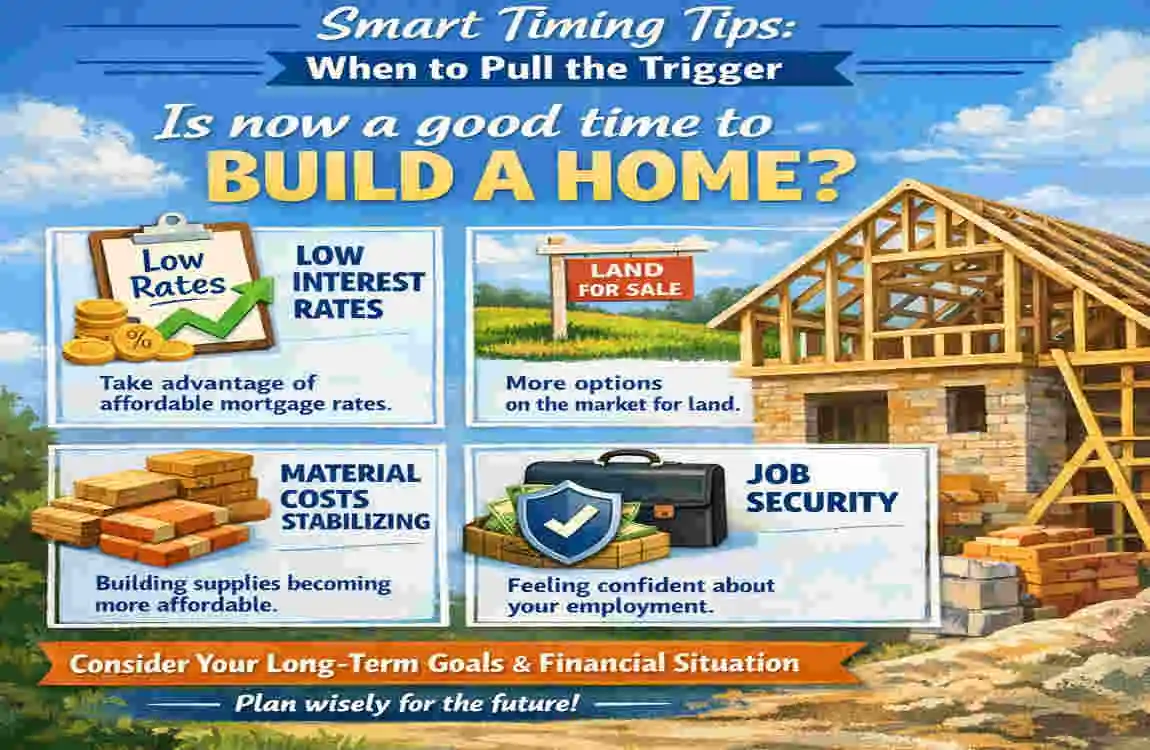

Smart Timing Tips: When to Pull the Trigger

Okay, you have weighed the pros and cons. You are still interested. Now the question shifts from “should I” to “when should I?”

Timing is everything. Here are four smart tips to help you decide when the answer to “Is now a good time to build a home?” is a definitive “Yes.”

Monitor Economic Indicators

You don’t need to be an economist, but you should pay attention to the news. Specifically, keep an eye on the Federal Reserve meetings and CPI (Consumer Price Index) reports.

If inflation is trending down, mortgage rates usually follow. The best window to lock in a construction loan is often in the Spring, just before the busy summer building season starts. If you see rates dip below 6.5%, that is your signal to get pre-approved immediately.

Assess Personal Finances First

Forget the market for a second. Look at your bank account. Building a house is stressful; being “house poor” makes it unbearable.

Before you sign a contract, ensure your debt-to-income (DTI) ratio is below 36%. Lenders for construction loans are stricter than standard mortgages.

You should also aim to have 20% down saved, plus a cash reserve of at least 10% of the total build cost for overages. If you don’t have that cushion, wait a few months and keep saving.

Choose the Right Location and Builder

You can change the paint, but you cannot change the location. Look for areas with planned infrastructure improvements, such as new schools, hospitals, or transit lines. These are indicators of future value growth.

When it comes to builders, do not just go with the cheapest bid.

- Check their reviews from 2024 and 2025.

- Ask to see the current active job sites. Are they messy? Are they moving?

- Vetting your builder is the single most important step to preventing a nightmare scenario.

Future-Proof Your Build

If you are going to build in 2026, build for the future.

Consider modular or prefab construction. These homes are built in factories and assembled on-site. They can save you up to 20% on costs and months on the timeline because the weather doesn’t delay the framing process.

Also, integrate smart home technology. Hardwiring for security, high-speed data, and smart thermostats significantly increases resale value.

Who Should Build Now vs. Wait? Quick Decision Guide

Still on the fence? Let’s simplify this. Real estate is personal. What works for your neighbor might be a disaster for you.

Here is a quick guide to help you decide whether it is now a good time to build a home for your specific situation.

Build Now If:

- You have stable employment: You are confident your income won’t drop in the next 2 years.

- You already own land: This removes a huge chunk of the upfront cost and risk.

- Customization is a deal breaker: You have specific needs (accessibility, large family, home business) that existing inventory cannot meet.

- You plan to stay 7+ years: This allows you to ride out any short-term dips in market value.

Wait If:

- Your budget is tight: If you are scraping together the down payment, a construction project will likely bankrupt you.

- You need to move fast: If you have a baby on the way in 3 months or a job transfer, building takes too long.

- You are terrified of recession: If market volatility keeps you up at night, buy a move-in-ready home for peace of mind.

Decision Matrix

Scenario Build Now? Why?

Interest Rates Falling Yes Lock in equity early, refinance later.

Recession Looming: Preserve your cash reserves.

Family Growing Fast Yes, You need custom space that fits your life.

Job Market Volatile . No , too much risk with a long-term loan.

Here is a short, punchy FAQ section tailored for your blog at homeimprovementcast.co.uk. It is written in a conversational style to keep your readers engaged while answering their most pressing questions about the 2026 market.

Frequently Asked Questions: Is Now a Good Time to Build a Home?

Is now a good time to build a home in 2026?

Generally, yes. While interest rates aren’t at historic lows, material costs for lumber and concrete have stabilized significantly compared to the post-pandemic peaks. If you have a healthy down payment and plan to stay in the home for 7+ years, building now allows you to avoid the bidding wars of the existing resale market and gain immediate equity through modern, energy-efficient designs.

Is it cheaper to build or buy a house right now?

In most cases, buying an existing home is cheaper upfront. Building a custom home typically costs 15% to 25% more than buying a similar existing property because you are paying for brand-new materials, labor, and land preparation. However, existing homes often come with “hidden” renovation costs (new roof, updated kitchen) that a new build does not have.

Will construction costs go down in 2027?

It is unlikely. While material prices have flattened out, labor costs are continuing to rise due to a shortage of skilled tradespeople (plumbers, electricians, framers). Waiting for costs to drop might actually cost you more in the long run if labor shortages worsen.

How long does it take to build a house in 2026?

You should budget for 9 to 12 months on average for a custom home. While supply chains are flowing smoothly again, the labor shortage means you might wait longer for subcontractors to become available. Always add a 2-month buffer to your timeline for weather delays or permitting hiccups.

Should I wait for interest rates to drop further?

Trying to time the market is risky. While rates might dip slightly, most experts predict they will stay in the 6% range for the near future. The smart move is to “marry the house and date the rate.” If you build now, you can enjoy your home immediately and simply refinance later if rates take a significant dive.

What is the very first step I should take?

Before you look at floor plans or land, talk to a lender who specializes in construction loans. These are different from standard mortgages. You need to know your exact budget—including a 10-15% contingency fund for unexpected costs—before you fall in love with a design you cannot afford.