If you have ever wondered what the difference is between a chattel and a house, you are not alone. This question comes up a lot in real estate because the words sound simple, but the legal meaning can be very different. In a home sale, one small misunderstanding can lead to stress, delays, or even a dispute after closing.

The main issue is this: a house is usually part of the land, while chattel is movable personal property. That difference affects ownership, taxes, insurance, financing, and what stays behind when a property is sold. A buyer may think an appliance is included, while the seller may see it as something they can take with them.

So, if you are buying or selling a home, it helps to know the rules early. Understanding the difference between chattel and house protects your money and avoids surprises. It also makes contracts clearer, which is always a smart move in real estate.

Understanding the Basic Definitions

What Is a House in Real Estate?

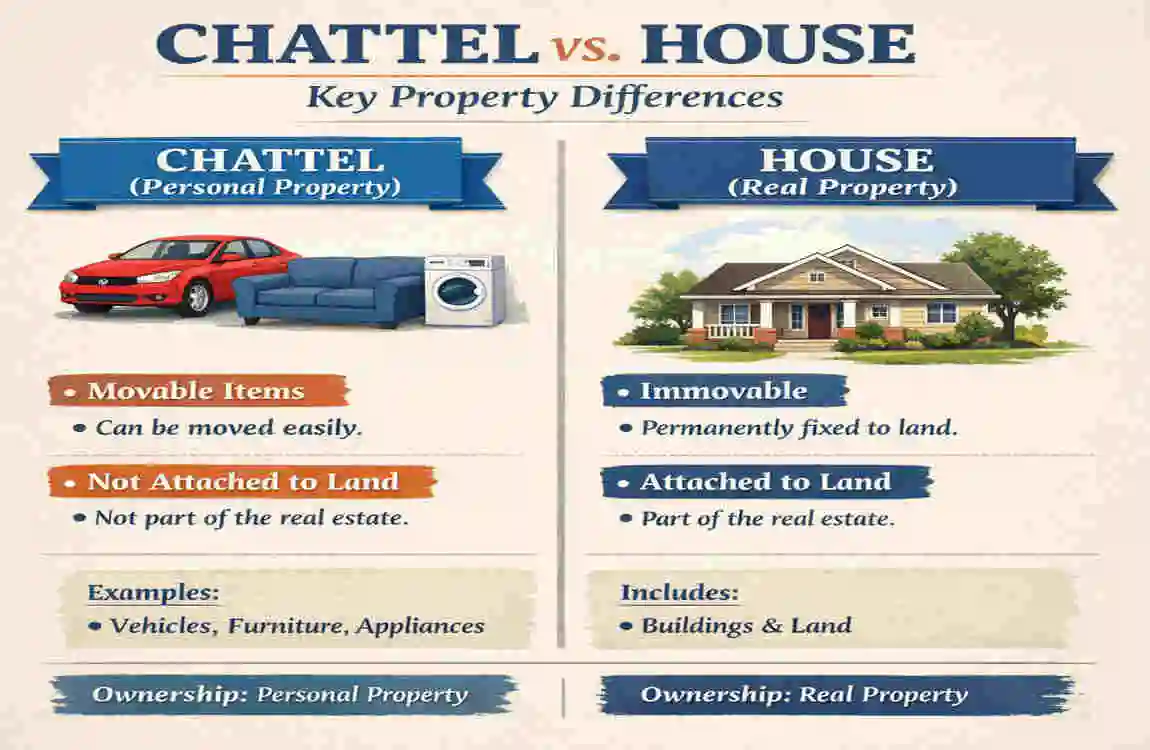

A house is usually considered real property. That means it is a permanent structure attached to land. In simple terms, the land and the building are treated as one legal asset.

A house is not easy to move. It is built to stay in one place, often on a foundation. That is why single-family homes, duplexes, and condominiums are normally treated as real estate. They are tied to the land in a lasting way.

What Is Chattel?

Chattel is personal property that can be moved. It is not permanently attached to the land. If you can remove it without damaging the property, it may count as chattel.

Common examples include furniture, portable appliances, curtains, and other movable items. In real estate, the term “chattel” usually refers to items that are not part of the land itself.

The Legal Difference Between Chattel and a House

Real Property vs Personal Property

The biggest legal difference is simple:

- A house is real property

- Chattel is personal property

That difference matters because ownership is handled differently. Real property ownership usually transfers through a deed. In contrast, chattel may be transferred through a separate bill of sale or a written agreement.

Why the Law Treats Them Differently

The law separates them for several reasons. Taxes are one of the biggest. A house may be taxed as part of real estate, while chattel may be taxed differently, or not at all, depending on the item and location.

Financing is another major issue. A house can usually be financed with a traditional mortgage. Chattel may need a different type of loan, especially if it is a mobile home or manufactured home.

There are also estate planning and title issues. If someone passes away, real property and personal property may be handled differently. That is why clear classification matters.

The “Fixture Test” in Real Estate

Sometimes an item sits in a gray area. Courts and real estate professionals use a fixture test to decide whether something is part of the house or still chattel.

They usually look at four things:

- How firmly it is attached

- Why was it attached

- Whether removal would cause damage

- Whether the item was meant to stay permanently

For example, a built-in dishwasher is often considered part of the house. A portable dishwasher is more likely to be chattel. A wall-mounted TV may be treated differently from a freestanding TV, depending on the contract and installation.

Key Characteristics That Set Chattel Apart from a House

Permanence

A house is built to last in one place. It does not move easily, and that permanence is part of its legal identity.

Chattel, on the other hand, is movable. It can be carried, transported, or removed without changing the land itself.

Mobility

This is one of the easiest ways to tell the difference. If an item can be moved from place to place, it is usually chattel. If it is fixed to the land or the structure, it may be part of the house.

This is why the phrase “movable property” is often used when referring to chattel.

Ownership Rights

Ownership rights can be different, too. A house usually transfers with the sale of the land. Chattel may need to be listed separately if the buyer expects to receive it.

That is why real estate contracts should be clear. If something matters to the deal, it should be written down.

Financing and Insurance

A house usually qualifies for a house mortgage. Chattel often does not.

This matters a lot for items like:

- Mobile homes

- Manufactured homes

- RVs

- Some temporary structures

These may require chattel financing rather than a standard mortgage. Insurance can also differ. Homeowner’s insurance often covers a luxury house, while chattel may need special coverage.

Common Examples of Chattel in Real Estate Transactions

Household Items Considered Chattel

Many everyday items are usually chattel, such as:

- Sofas

- Beds

- Lamps

- Washing machines

- Freestanding refrigerators

These are typically not attached permanently, so they are easy to remove.

Items Commonly Considered Part of the House

Some items are usually treated as part of the home, including:

- Cabinets

- Plumbing systems

- Built-in ovens

- Central HVAC systems

These are often attached permanently and intended to remain with the property.

Gray Areas That Cause Disputes

This is where problems often begin. Items like mounted mirrors, blinds, security systems, garden sheds, and smart home devices can be difficult to understand.

A buyer may assume they are included. A seller may think they are taking them. If the contract is not specific, disagreement can happen quickly.

Chattel vs Fixture: Why It Matters in Home Sales

Impact on Purchase Agreements

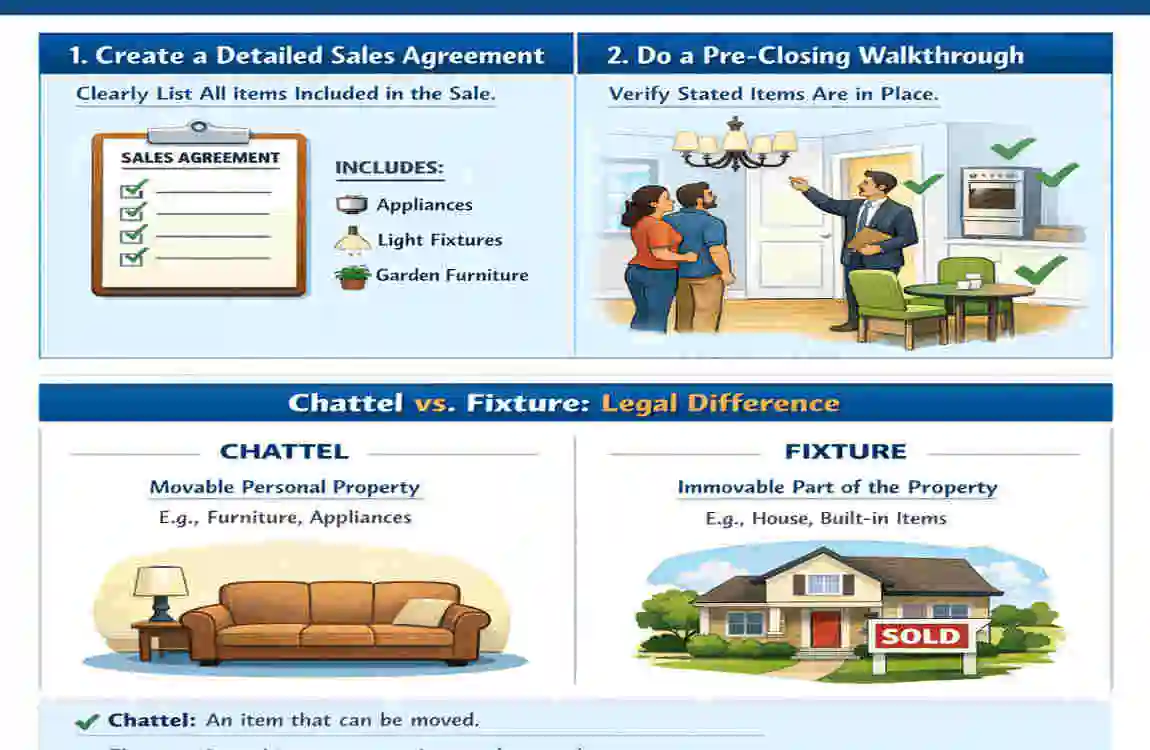

Real estate contracts should clearly say what is included in the sale. This is where the distinction between fixtures and chattels becomes very important.

If appliances, light fixtures, or window coverings matter to the buyer, they should be listed in writing. A simple verbal promise is often not enough.

Buyer Expectations vs Seller Intentions

Buyers often assume that anything attached to the home stays. Sellers may see certain items as their personal property.

That difference in expectation causes many disputes. The best fix is simple: put everything in writing.

Legal Disputes After Closing

After closing, missing items can turn into home sale disputes. A seller might remove a light fixture or take an appliance the buyer thought was included.

To avoid that, buyers should:

- Do a final walkthrough

- Take photos of the included items

- Review the contract carefully

- Ask a real estate attorney if anything is unclear

Are Mobile Homes Chattel or Real Estate?

When a Mobile Home Is Considered Chattel

A mobile home is often treated as chattel when it is not permanently attached to land. If it can be moved and is still titled like a vehicle or personal asset, it may remain personal property.

When It Becomes Real Property

A mobile home may become real property if it is placed on a permanent foundation and tied to land ownership. In that case, it may be treated more like a traditional house.

Financing Differences

This difference affects manufactured home financing and mobile home financing. A chattel mortgage may have different interest rates and terms than a standard mortgage. So if you are buying one, check the loan type carefully.

Tax and Insurance Implications

Property Taxes on Houses

Houses are usually taxed as real estate. The tax often includes both the land and the structure.

Tax Treatment of Chattel

Chattel may be taxed differently. Some items may lose value over time through depreciation, especially business-use personal property.

Insurance Coverage Differences

Homeowner’s insurance usually covers a house. Chattel may need contents insurance or a special policy, depending on the item.

How Buyers and Sellers Can Avoid Chattel Disputes

Create Detailed Purchase Agreements

The easiest way to avoid problems is to list items clearly in the contract. If you want appliances, blinds, or fixtures to stay, write them in the agreement.

Conduct a Final Walkthrough

Before closing, walk through the property and confirm that everything agreed upon is still in place. This is your last chance to catch a problem early.

Consult Real Estate Professionals

Real estate agents, property lawyers, and mortgage advisors can help you understand what constitutes chattel and what constitutes part of the house. That guidance can save time and money.

Frequently Asked Questions

Is a refrigerator considered chattel or part of the house?

Usually, a freestanding refrigerator is chattel. But if it is built in, the answer may be different. The contract should always decide the final answer.

Can chattel become real property?

Yes. If chattel becomes permanently attached to the land or a structure, it may become a fixture and be treated as part of the house.

What happens if a seller removes fixtures after closing?

If the item was supposed to stay, the buyer may have a legal claim. This can lead to repair costs, replacement costs, or a dispute over the contract terms.

Are manufactured homes considered chattel?

Sometimes, yes. If they are not permanently attached to land, they are often treated as chattel. If they are fixed to a foundation and tied to the land, they may be real property.

Why does the distinction matter in mortgages?

Because lenders treat houses and chattel differently, a house often qualifies for a traditional mortgage. In contrast, chattel may need a chattel mortgage or another type of loan.

Do all appliances count as chattel?

No. Some do, and some do not. A freestanding appliance is often chattel, while a built-in appliance may be treated as part of the home.

| Feature | Chattel | House (Real Property) |

|---|---|---|

| Definition | Movable personal property not part of the land | Permanent structure attached to land |

| Attachment | Not permanently fixed; can be removed without damage | Permanently built/fixed to the land |

| Ownership in Sale | Not automatically included; must be specified in contract | Automatically included in property sale |

| Examples | Furniture, freestanding appliances, curtains, rugs, garden benches | Building itself, built-in cabinets, fixed floors, plumbing, wiring |

| Legal Classification | Personal property (movable asset) | Real property (real estate) |

| Removal Impact | Can be taken by seller without damaging property | Cannot be removed without destroying part of the property |