you have finally decided to sell your home. You cleaned every room, staged your furniture perfectly, and hosted open houses. Suddenly, your real estate agent calls with fantastic news. You have received an offer, you negotiated the terms, and you both signed on the dotted line. You are officially on your way to closing the deal!

However, as the initial thrill settles down, a very common question probably pops into your mind. How long can a house be under contract before the deal is completely finalized?

When you sit around waiting for updates, the days can feel incredibly long. You might wonder if things are moving too slowly or if the buyer is going to back out. The truth is, the period between accepting an offer and actually handing over the keys involves several moving parts. From securing a mortgage to passing a home inspection, each step takes a specific amount of time.

What Does “Under Contract” Really Mean?

Before we dive into the specific timelines, we need to clarify what this terminology actually means. Real estate jargon sometimes feels like a completely different language, especially if you are a first-time seller or buyer. Let us break down the legal basics into understandable segments.

The Legal Basics Explained Simply

When someone says a property is “under contract,” it means the seller has accepted an offer from a buyer, and both parties have signed a formal purchase agreement. This signed document is a legally binding contract.

However, the sale is not final yet. The contract usually comes with specific conditions, known as contingencies. These contingencies are basically safety nets. They allow the buyer to legally back out of the deal if certain expectations are not met. For example, if the home inspection reveals massive structural damage, the buyer can walk away without losing their initial deposit.

Think of being under contract like being engaged. You have made a serious commitment to each other, but you are not officially married until you sign the marriage certificate on your wedding day. In real estate, that wedding day is your closing day.

Signed Agreement vs. Pending Status

You might also hear the term “pending” thrown around. While people often use “under contract” and “pending” interchangeably, they can mean slightly different things depending on your local real estate listing service.

Generally, a house is under contract the moment the paperwork is signed. It remains in this status while the buyer works through their contingencies, such as getting their mortgage approved or completing the property inspection.

A home usually moves to a pending status once all those contingencies have been met and successfully cleared. At this point, the deal is very close to the finish line, and it is highly unlikely that the transaction will fall through.

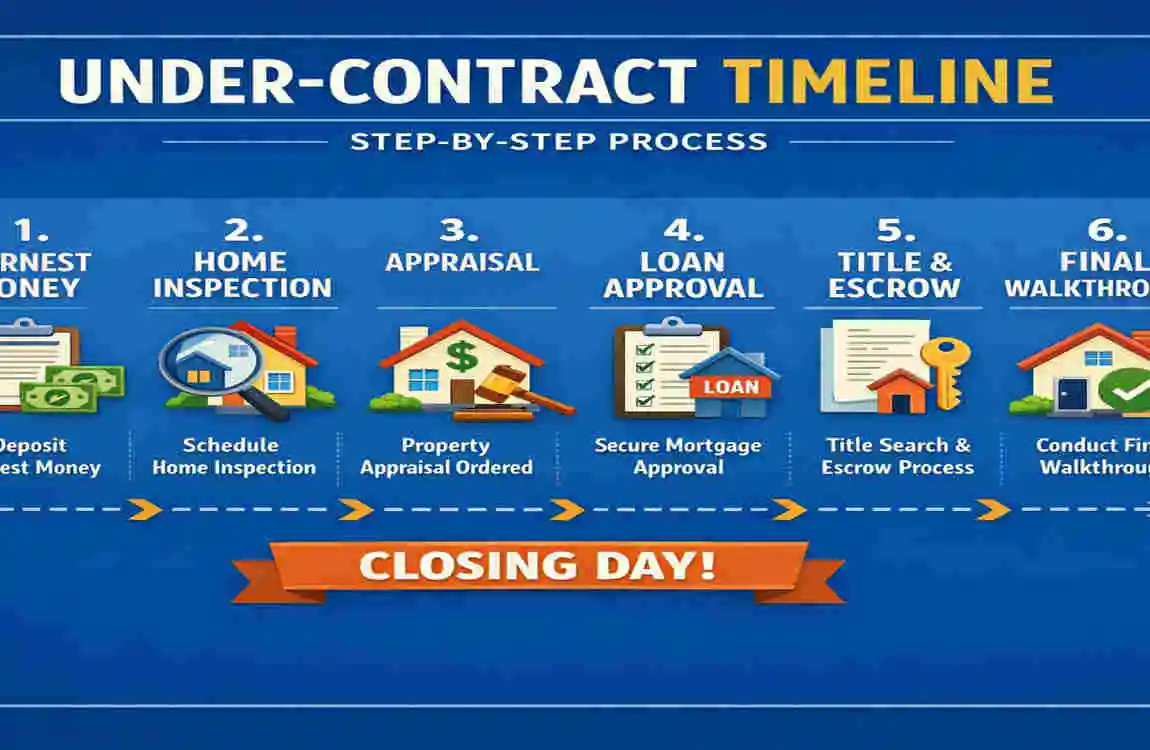

The Core Phases from Offer to Closing

To understand how long a house stays under contract, you need to look at the core phases of the process. The journey from accepting the offer to officially closing involves several key milestones.

First, the buyer deposits their earnest money, which shows they are serious about the purchase. Next comes the inspection phase, where professionals evaluate the home’s condition. Following that is the appraisal, where the lender confirms the home’s value. Finally, the buyer’s lender must finalize the financing.

The timeline for these steps can vary widely based on regional norms. For instance, the traditional closing timeline in the United States might look very different from the standard practices. Understanding these phases will help you navigate the waiting period with much less stress.

Typical Timelines: How Long Can a House Be Under Contract on Average?

Now, let us answer the core query directly. You want to know the exact numbers so you can plan your move, organize your finances, and prepare for your next chapter.

The Standard 30 to 60-Day Window

If you look at the national averages, particularly in regions like the United States, a typical house under contract timeline ranges from 30 to 45 days in very hot markets. In more standard, balanced markets, you are looking at a 45 to 60-day window.

Why does it take a month or two to finalize a sale? The answer lies in the paperwork and the verification processes. When a buyer requires a mortgage to purchase your home, the bank needs time to ensure it is making a safe investment.

Key Factors That Influence Your Timeline

Several primary factors dictate exactly how long a house can be under contract. Let us look at the most time-consuming elements of the process.

First is buyer financing. Securing a mortgage is usually the longest part of the journey. The buyer’s lender needs to review tax returns, verify employment, and scrutinize credit histories. This underwriting process typically takes 30 to 45 days to complete.

Next up are home inspections and appraisals. Scheduling an inspector, conducting the inspection, and negotiating any necessary repairs usually eats up 7 to 14 days. After that, the bank will send an appraiser to value the property, which can add another week to the timeline.

Finally, you have title searches and title insurance. A title company must research the property’s history to ensure there are no hidden liens, unpaid taxes, or legal claims against the house. This necessary legal safeguard generally takes 10 to 20 days.

Visualizing Timelines by Market Type

To give you a clearer picture, here is a helpful breakdown of typical durations based on the type of real estate market you are currently navigating.

Market Type: Typical Duration: Examples

Seller’s Market 21-30 days Hot urban areas like prime

Balanced Market 30-45 days Standard family homes in quiet neighborhoods

Buyer’s Market 45-60+ days Rural properties or homes needing major renovations

2026 Real Estate Trends Impacting Timelines

It is also vital to consider the current economic climate. As we navigate through 2026, we are seeing some unique trends that affect the pending sale duration.

For instance, fluctuating interest rates have caused lenders to become slightly more cautious. This extra scrutiny means the underwriting process is taking longer than it did a few years ago. In many cases, these strict lending regulations are extending standard timelines by about 10% to 15%.

Staying aware of these modern market shifts helps you set realistic expectations from the very beginning of your transaction.

Step-by-Step Breakdown of the Under-Contract Timeline

If you want to truly grasp the typical house under contract timeline, it helps to walk through the process day by day. Breaking this complex journey into understandable segments will show you exactly what happens behind the scenes while you wait.

Days 1 to 3: The Offer Acceptance

The clock officially starts ticking the moment both the buyer and the seller sign the purchase agreement. This is a very busy initial period.

During these first three days, the buyer is required to submit their earnest money deposit. This money is usually held in a secure escrow account by a neutral third party. This deposit acts as a show of good faith, proving that the buyer is genuinely committed to purchasing your property.

At the same time, the buyer will send the fully executed contract to their mortgage lender to officially kick-start the loan approval process. Your real estate agent will also update the property’s status on the local listing service to show that it is now under contract.

Days 4 to 14: The Contingency Period

The next week and a half is usually dedicated to the contingency period. This is when the buyer performs their due diligence to ensure the house is in the condition they expect.

The buyer will hire a professional home inspector to examine the property thoroughly. The inspector will check the roof, the foundation, the electrical systems, and the plumbing. If the inspector finds significant issues, the buyer might ask you to make repairs, or they might ask for a reduction in the sale price to cover the cost of fixing things themselves.

During this same window, the lender will order a home appraisal. The appraiser visits your home to determine its fair market value. The bank wants to guarantee that the house is actually worth the amount of money they are lending to the buyer. If the appraisal comes in lower than the agreed-upon purchase price, you and the buyer will have to negotiate a solution.

Days 15 to 30: Financing and Underwriting

Once the inspections and appraisals are cleared, the focus shifts entirely to the buyer’s finances. This is known as the underwriting phase.

The lender’s underwriter will painstakingly review the buyer’s financial background. They will double-check bank statements, verify ongoing employment, and ensure the buyer has not taken on any new massive debts, like buying a new car.

As a seller, this phase can feel incredibly quiet. You might not hear from your agent for days at a time. Do not panic! Silence is often a good thing during underwriting. It simply means the lender is doing their paperwork and moving the loan toward final approval.

Days 31 to 45: Final Walkthrough and Title Clearance

As you enter the second month, the finish line comes into view. During this phase, the title company completes its extensive search of public records. They want to make absolutely sure that you have the clear, legal right to sell the property and that no one else can claim ownership.

Once the title is cleared and the lender issues a “clear to close” status, the buyer will schedule a final walkthrough. This usually happens a day or two before the closing date.

The buyer will walk through your empty house to ensure it is in the same condition it was when they made the offer. They will also verify that you have completed any repairs you agreed to during the inspection phase.

Day 46 and Beyond: Closing Day

Finally, closing day arrives! This is the day you have been waiting for since you first listed your home.

You and the buyer will sign a massive stack of legal documents. Once all the paperwork is signed and notarized, the buyer’s lender will wire the purchase funds to the title company or closing attorney.

After the funds are successfully transferred and the transaction is officially recorded with the local government, you will hand over the keys. The house is no longer under contract; it is officially sold!

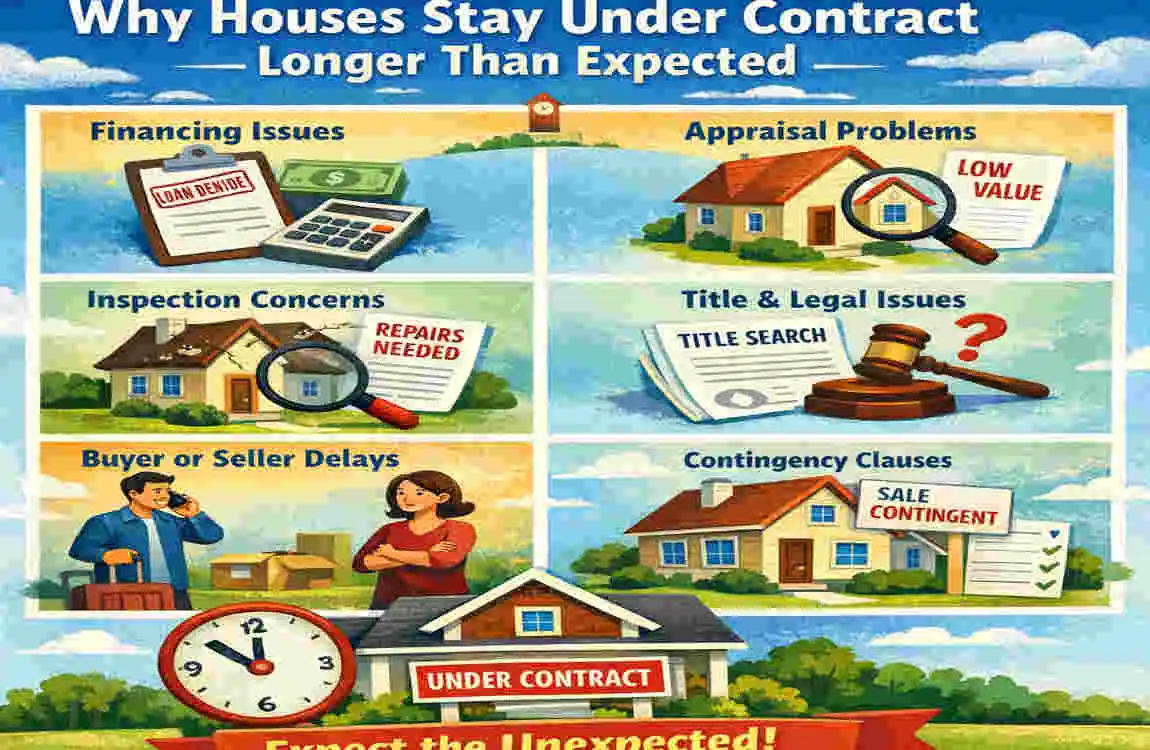

Common Reasons for Contract Extensions and How They Work

In a perfect world, every real estate transaction would follow that timeline flawlessly. However, real life is rarely perfect. Sometimes, the initial closing date comes and goes, leading people to search for information on a real estate contract extension.

What Triggers a Real Estate Contract Extension?

Extensions are incredibly common in the real estate industry. They happen when one or both parties need a little more time to fulfill their contractual obligations. But what exactly causes these delays?

One major trigger is a failed or problematic home inspection. If the inspector discovers a major issue, like a faulty electrical panel or a leaking roof, the buyer might demand that you fix it before closing. Finding a reliable contractor and getting the work done takes time, which pushes back the closing date.

Another frequent culprit is the appraisal gap. If the bank appraises the home for less than the purchase price, the buyer’s lender will not cover the difference. The buyer and seller must then take time to renegotiate the price or figure out how to cover the cash shortfall.

Finally, lender delays are incredibly common. Sometimes, an underwriter asks for additional financial documentation at the last minute, which stalls the final loan approval.

The Typical Length of an Extension

So, if you run into a hiccup, how long does a real estate contract extension usually last? In most cases, extensions are granted for anywhere between 7 and 30 days.

The exact length depends entirely on the problem at hand. If the lender needs a few extra days to process paperwork, a one-week extension is usually sufficient. However, if you need to replace the entire roof before the buyer’s lender will approve the loan, you might need a full 30-day extension to complete the construction.

The Pros and Cons of Extending

When faced with a delay, you might wonder if extending the contract is the right move. Like most things in real estate, there are pros and cons to this decision.

The biggest advantage of signing an extension is that it keeps the current deal alive. You do not have to put your house back on the market, host more open houses, and start the stressful search for a new buyer from scratch. It saves you a tremendous amount of time and energy.

The downside is that it extends your waiting period. It also carries a slight risk. Sometimes, an extension gives a skittish buyer more time to second-guess their purchase, increasing the chance that they might try to find a loophole to back out entirely.

The Legal Must-Haves for Extending a Contract

You cannot simply agree to an extension over a quick phone call. A real estate contract extension must be handled legally and formally.

Your real estate agent will draft a document called an addendum. This written notice outlines the new agreed-upon closing date and explains the reason for the delay. Both the buyer and the seller must sign this addendum for it to be legally binding.

In some competitive scenarios, a seller might ask for a fee or an additional earnest money deposit to grant a lengthy extension. For example, a prime that was under contract recently extended its timeline by 14 days due to heavy monsoon-related roof repairs. The buyer agreed to the extension, and both parties signed an addendum to protect their interests while the repairs were completed.

Potential Delays: Why Houses Stay Under Contract Longer Than Expected

To truly build your real estate expertise, you need to understand the pitfalls that cause delays. Knowing why houses stay under contract longer than expected helps you prepare for the worst while hoping for the best.

The Top Culprits Behind Closing Delays

When a closing date gets pushed back, it is rarely a surprise to the professionals involved. Certain issues pop up time and time again.

According to industry data, financing issues are the biggest hurdle, accounting for roughly 35% of all delayed closings. Buyers sometimes make the mistake of opening a new credit card or missing a bill payment during the underwriting phase, which throws their entire mortgage application into chaos.

Low appraisals are the second most common problem, causing about 20% of delays. In rapidly changing markets where home prices fluctuate, appraisers sometimes struggle to find recent, comparable sales to justify a high purchase price.

Title problems make up roughly 15% of delays. A title search might reveal an old contractor’s lien that was never officially cleared, or a dispute over property boundary lines that must be legally resolved before the sale can proceed.

Navigating Supply Chain and Lending Regulations in 2026

As we look at the real estate landscape in 2026, we see some modern factors adding extra days to the standard contract timeline.

Supply chain issues continue to linger in the construction and home repair industries. If your home inspection reveals that you need a specific type of replacement window or a new HVAC unit, you may be waiting weeks for the parts to arrive. These material shortages force sellers to ask for longer extensions to complete agreed-upon repairs.

Furthermore, post-2025 financial regulations have made mortgage lenders much stricter. Banks are requiring more documentation and taking extra time to verify employment stability. These tighter lending rules mean that even highly qualified buyers are experiencing slightly longer underwriting periods.

The Reality of Contracts Falling Through

While we always aim for a successful closing, it is important to be realistic. Sometimes, delays become insurmountable roadblocks.

Current data suggests that about 10% to 15% of all real estate contracts eventually expire or terminate without resulting in a closed sale. Whether it is a buyer losing their job right before closing or a home inspection uncovering disastrous foundation issues, some deals cannot be saved. Knowing this reality highlights why it is so crucial to monitor your timeline closely.

When Does “Under Contract” End? Expiration, Termination, and Backup Offers

At some point, the pending phase has to conclude. But how exactly does this period end if you do not make it to the closing table? Let us explore how contracts expire, how they are terminated, and how you can protect yourself.

Understanding Contract Expiration

Every real estate purchase agreement includes a specific closing date. If that date arrives and the transaction is not completed, and neither party has signed a formal extension addendum, the contract essentially expires.

Furthermore, contracts have specific timelines for their contingencies. For example, your contract might include a 45-day financing clause. If the buyer cannot secure their mortgage approval within those 45 days, the contingency expires. At this point, the seller has the legal right to walk away from the deal and put the house back on the market.

Termination Options for Buyers and Sellers

Expiration is a matter of time running out, but termination happens when someone actively chooses to cancel the agreement.

If a buyer uses a valid contingency to walk away—like refusing to buy the house after a terrible inspection—they terminate the contract legally. In this scenario, they are usually entitled to get their earnest money deposit back.

However, if a buyer gets cold feet and decides to walk away without a valid contractual reason, this is considered a buyer’s default. When a buyer defaults, the seller generally has the right to terminate the contract and keep the earnest money deposit as compensation for the time their house was off the market.

If both parties agree that the deal is no longer working out, they can sign a mutual release document. This legally terminates the contract and outlines exactly how the earnest money will be divided or returned.

The Smart Strategy of Accepting Backup Offers

As a seller, you might feel vulnerable while your house is locked up in a contract. What happens if the deal falls through after 45 days? You have lost a month and a half of valuable marketing time!

This is why smart sellers accept backup offers. Even when you are under contract with a primary buyer, you can still allow other interested buyers to view the home and submit offers.

If you receive a great backup offer, you can accept it in a secondary position. This means that if your primary contract falls through, your backup buyer automatically slides into the first position.

Here is a pro tip: ask your real estate agent to list your property as “active under contract” or “accepting backups” on the local listing service. This tells the market that while you have an accepted offer, you are still open to entertaining other serious buyers.

Expert Tips to Shorten Your House Under Contract Timeline

Nobody wants to sit in limbo for three months. If you want to get to the closing table as quickly as possible, you need to be proactive. Here are some actionable, expert tips to help you shorten your timeline.

Proactive Steps You Can Take Today

Taking control of your sale starts before you even accept an offer. By preparing in advance, you can eliminate the most common roadblocks that cause painful delays.

Here is a list of strategies you can implement to speed up your transaction:

- Pre-inspect your home: Do not wait for the buyer to find problems. Hire a home inspector before you list your property. Fix the leaky pipes, repair the roof shingles, and update the electrical outlets in advance. This ensures the buyer’s inspection goes smoothly, completely eliminating the need for repair negotiations and extensions.

- Price realistically for quick appraisals: If you price your home far above its actual market value, the bank’s appraisal will come in low. This causes massive delays as you try to renegotiate. Price your home accurately based on recent comparable sales to ensure the appraisal clears without a single hiccup.

- Choose cash buyers when possible: If you receive multiple offers, strongly consider a cash offer, even if it is slightly lower than a financed offer. Cash buyers do not need mortgage underwriting or bank appraisals. This means a cash transaction can often close completely in just 7 to 14 days!

- Use digital tools for faster documentation: Work with a real estate agent and closing team that utilizes modern technology. Using electronic signatures, secure digital document sharing, and remote online notarization can shave days off the administrative timeline, keeping the process moving forward rapidly.

FAQs: How Long Can a House Be Under Contract?

We have covered a lot of ground, but you might still have a few specific questions lingering in your mind. Let us address the most frequently asked questions regarding the pending sale duration to ensure you have total clarity.

How long can a house be under contract before closing?

In standard residential real estate transactions, a house is typically under contract for 30 to 60 days before the closing is finalized. This gives the buyer enough time to secure their mortgage, complete the home inspection, and have the property officially appraised by the lender. However, cash sales can close much faster, often in just two weeks.

Can you extend a real estate contract?

Yes, absolutely. You can extend a real estate contract if both the buyer and the seller agree to the new terms. This is done by signing a legal document called an addendum. Extensions are very common and are typically used to give buyers more time to resolve financing delays or to give sellers more time to complete agreed-upon property repairs before closing.

What happens if the house under contract falls through?

If the deal falls through, the contract is officially terminated. Depending on the reason for the termination, the buyer will either receive their earnest money deposit back (if they used a valid contract contingency) or they will forfeit the money to the seller (if they defaulted). Once the contract is voided, the seller is free to put the house back on the active market and search for a new buyer.

What is the average pending sale time in 2026?

As we navigate 2026, the average pending sale time is hovering right around 45 to 50 days. Stricter lender regulations and ongoing supply chain issues for home repairs have slightly extended the standard timelines. Working with proactive real estate professionals is more important now than ever to keep your deal on track.